How Elon Musk Found is about to Steal from Your 401(k)

Why SpaceX's $1.77 trillion IPO will be force-purchased by your retirement fund — and what you can still do to stop it

It takes time to create work that’s clear, independent, and genuinely useful. If you’ve found value in this newsletter, consider becoming a paid subscriber. It helps me dive deeper into research, reach more people, stay free from ads/hidden agendas, and supports my crippling chocolate milk addiction. We run on a “pay what you can” model—so if you believe in the mission, there’s likely a plan that fits (over here).

Every subscription helps me stay independent, avoid clickbait, and focus on depth over noise, and I deeply appreciate everyone who chooses to support our cult.

PS – Supporting this work doesn’t have to come out of your pocket. If you read this as part of your professional development, you can use this email template to request reimbursement for your subscription.

Every month, the Chocolate Milk Cult reaches over a million Builders, Investors, Policy Makers, Leaders, and more. If you’d like to meet other members of our community, please fill out this contact form here (I will never sell your data nor will I make intros w/o your explicit permission)- https://forms.gle/Pi1pGLuS1FmzXoLr6

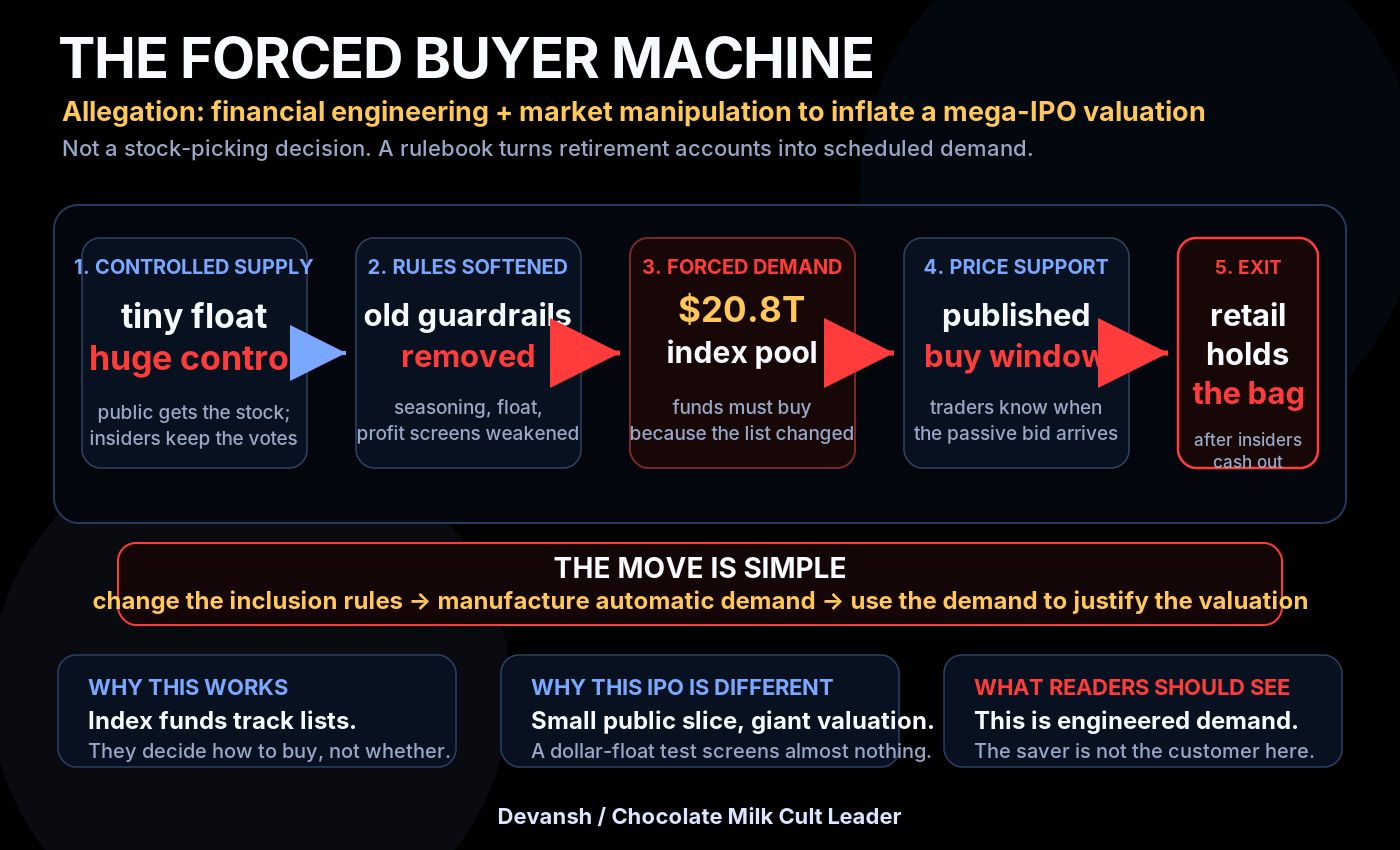

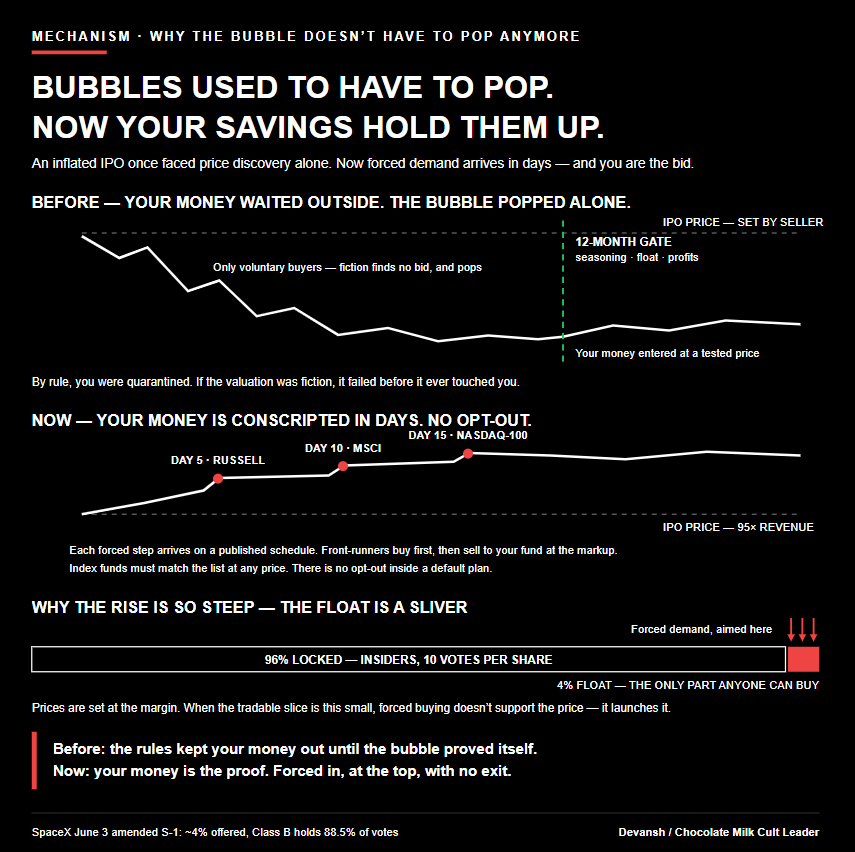

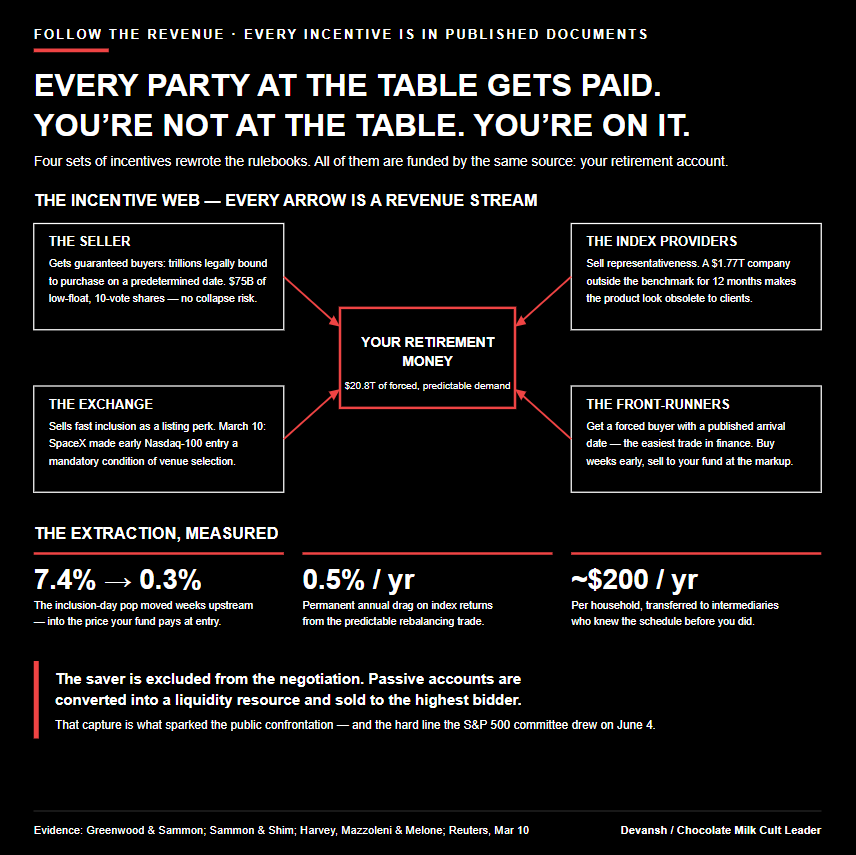

On Friday, June 12, 2026, SpaceX begins trading on Nasdaq. Within twenty business days, money from millions of automatic retirement accounts will buy the stock on a rigid, pre-published schedule. Nobody — not your fund manager, not you — gets to evaluate the company first.

Here is what’s being forced into your portfolio. SpaceX is selling roughly $75 billion of stock at a $1.77 trillion valuation — 95 times last year’s revenue, for a company that lost $4.9 billion doing it. The shares your retirement account buys carry one vote each; the shares insiders keep carry ten. After the sale closes, insiders control 88.5% of all voting power and Elon Musk alone commands 82.4%. And because an index fund must buy the complete corporate ledger, you can’t take the profitable Starlink business without also taking a cash-burning rocket division, the social platform X, and an AI venture that spent $12.7 billion on data centers in 2025 alone.

To help you understand how we got here — and what you can still do about it — this article will cover:

Which index benchmarks are buying SpaceX and on what schedule. Russell funds buy at the close of Day 5. MSCI global funds finalize by Day 10. Nasdaq-100 funds force entry after Day 15. We’ll map every fund family to its forced-purchase date so you can find your own exposure.

How the algorithmic front-running of these schedules drains $16 billion a year from passive investors. The purchase dates are published in advance and you can’t change them. Traders who know exactly when $14.4 trillion in passive capital must buy get to set the price it buys at — roughly $200 a year out of every indexed household.

How the index guardrails were dismantled in 90 days. Seasoning windows, float minimums, profitability screens, and voting-rights floors were built over a decade to protect retail investors. Between February and June, Nasdaq, FTSE Russell, CRSP, and S&P each rewrote their rulebooks to waive them for sufficiently large listings.

Why the S&P 500’s June 4 “rejection” of SpaceX is security theater. The committee publicly kept its screens for the S&P 500 — and in the same document, quietly opened its own Total Market, Completion, and Dow Jones benchmarks to low-float listings. Worse, those side doors let an asset accumulate the trading history and float needed to walk through the front gate 12 months later.

What’s inside the S-1 your retirement account is buying. The full balance-sheet dissection: segment losses, the AI division’s capex run-rate, the bitcoin treasury, and the voting math.

What you can actually do to block forced entry. The specific fiduciary, regulatory, and shareholder levers — ERISA prudence queries, the DOL comment window, pension exclusion mandates, and Rule 14a-8 proposals — including a template you can send to your plan committee today.

Executive Highlights (tl;dr of the article)

For this article, you might need to understand the following terms:

Index / benchmark: A published list of stocks with a rulebook deciding what gets in. Your index fund is legally bound to copy this list. Whoever writes the rulebook controls what your retirement account buys.

Passive fund: A fund that automatically buys whatever its index says, in the proportions it says, on the schedule it says. No human judgment in the loop. ~$14.4 trillion of American savings works this way, including most 401(k) default options.

Float: The percentage of a company’s shares actually available for the public to buy. SpaceX is floating 4.15% — insiders keep the rest. Low float means a thin sliver of trading sets the price for the whole company, so prices swing violently and insiders keep control.

Float minimum: The old guardrail requiring ~10% float before a stock could enter an index. This is the rule that was rewritten: now a float of any percentage qualifies if it’s worth enough raw dollars.

Seasoning window: A mandatory waiting period (typically 12 months) between a company going public and entering an index — time for hype to cool, lockups to expire, and real financial data to accumulate before your money is forced in.

Profitability screen: The requirement that a company show actual accounting profits before index entry. SpaceX lost $4.9 billion last year.

Dual-class shares: Two share types with unequal votes. Your shares: 1 vote. Insider shares: 10 votes. This is how Musk keeps 82.4% control while selling you the downside.

Rebalancing / forced buying: When the index list changes, every fund tracking it must buy or sell to match — at a published time, regardless of price. Predictable forced buying is what front-runners feed on.

Front-running: Buying a stock ahead of forced buyers you know are coming, then selling it to them at a markup. Legal when the schedule is public. This schedule is public.

Once you understand these terms, here is your tldr —

SpaceX Valuation and Forced Buying: On June 12, SpaceX begins trading at a $1.77 trillion valuation — 95x revenue with a $4.9B net loss. Within 20 business days, index funds holding millions of Americans’ retirement savings are contractually forced to buy it. No asset evaluation occurs by you or your fund manager; the rewritten index rulebook decides the purchase automatically.

The $16B Capital Extraction: Forced buying schedules are published in advance, allowing traders to buy the stock early and sell it back to passive investors at marked-up prices. This mechanism drains roughly $16B a year from passive investors (~$200 per indexed household). Research confirms that these fast-tracked index additions underperform by 22% over the following year, forcing index funds to buy at the top.

Dismantling Investor Guardrails: Four index providers removed protections like seasoning windows, float minimums, profitability screens, and voting floors within 90 days. They replaced percentage-based protections with raw dollar thresholds, allowing massive companies to bypass safety rules. These changes specifically target the largest listings; one provider’s consultation explicitly named “SpaceX, OpenAI, Anthropic” as the motivation.

S&P 500 Security Theater: The S&P 500’s June 4 rejection of these changes is a brand stunt. The same document opened S&P’s total-market benchmarks to low-float listings, feeding growth, ESG, and target-date products automatically. This creates a side-door where a company accumulates the required trading history over 12 months to enter the S&P 500 front gate later.

The Toxic Inside Bundle: The forced bundle forces you to buy profitable Starlink alongside a loss-making rocket division, X, and an AI venture with capex exceeding its revenue. Elon Musk retains 82.4% control via 10:1 insider voting shares, leaving shareholders with mandatory arbitration instead of court access.

The Retirement Exit Liquidity Pipeline: This is the standard pipeline moving forward, not an isolated incident. Both Anthropic ($965B) and OpenAI ($852B) filed confidential S-1s within the past two weeks. If these rules stand, retail retirement capital becomes the permanent exit liquidity for private valuations forever.

Your Direct Leverage Actions: The index machine runs entirely on your paycheck deductions, giving you real leverage to fight back. You can audit your fund benchmarks, send an ERISA prudence query to your 401(k) committee to force the issue onto the plan’s fiduciary records, and comment on the DOL’s safe-harbor rule. You can also push pension boards to exclude low-float multi-class listings and file shareholder proposals at index providers, replicating past participant litigation that cut 401(k) costs in half.

I put a lot of work into writing this newsletter. To do so, I rely on you for support. If a few more people choose to become paid subscribers, the Chocolate Milk Cult can continue to provide high-quality and accessible education and opportunities to anyone who needs it. If you think this mission is worth contributing to, please consider a premium subscription. You can do so for less than the cost of a Netflix Subscription (pay what you want here).

Want access to a repository containing all of our research? 300+ files containing our notes of various experiments, discussions with cutting-edge teams, and insights into where the industry is headed next. Get a Founding Member Subscription to AI Made Simple. Want to talk to me for details/get my insights into the tech ecosystem? Reach out to me through any of my socials over here or reply to this email.

Which Index Benchmarks Are Buying SpaceX and on What Schedule?

Every passive fund is legally bound to replicate an underlying benchmark owned by an independent company (and the same company might have 2 indexes that track 2 different benchmarks). For example, Vanguard’s Total Stock Market ETF (VTI) tracks the CRSP U.S. Total Market Index; the Vanguard Total World Stock ETF (VT) tracks the FTSE Global All Cap; Invesco’s QQQ tracks the Nasdaq-100. To find your exposure to Elon’s newest scam, you’ll have to look at the “seeks to track” statement on your fund’s official profile page.

Once you know your exposure, the next variable to track is the timing. The specific countdown to forced purchasing begins the moment SpaceX logs its first trade on Friday, June 12, 2026. Then you have to look out for the following:

Russell Large-Cap Funds: Forced buying occurs all at once at the market close on Day 5 — expected Thursday, June 18 — under a single-batch rule adopted by the committee on May 26.

MSCI Global Funds (ACWI, World): The fast-track inclusion decision is announced between Day 1 and Day 3, with mandatory buying finalized after the close of Day 10 — expected Friday, June 26.

Nasdaq-100 Funds (QQQ): The asset is evaluated on Day 7 and forced into the index after the close of Day 15 — early July 2026.

Total Market Funds: CRSP (governing Vanguard’s VTI complex) altered its design on April 27 to bypass percentage limits if an asset passes a raw dollar test. S&P’s total-market index series implemented an identical dollar-alternative clause alongside a five-day fast-track trigger on June 8.

Target-Date Funds: These vehicles automatically absorb the stock based on the underlying proportion of CRSP, Russell, Nasdaq, or MSCI products they hold internally.

These dates matter more than you think. Across the $14.4 trillion sitting in domestic passive equity funds, the general cost of running predictable, schedule-driven rebalancing trades already drains an estimated $16 billion annually from people due to algorithmic front-running. However, waiving float minimums for a mega-cap listing like SpaceX introduces an entirely new layer of volatility risk. When algorithmic traders know the purchase schedules ahead of time for a massive, low-float asset, the resulting price distortions will likely worsen this existing multi-billion-dollar drain on your savings.

Let me rephrase that clearly: since algorithmic traders know the purchase schedules ahead of time (which you can’t change since you can’t control the index), they can scalp your hard-earned savings (the phenomenon already costs people 16 Billion USD annually). You are the product being sold to convince Silicon Valley Elites and their bankers to invest in an overinflated bubble.

Maybe you’re wondering if this isn’t the way it’s always been. Or you think I’m reading too much into something. However, if you break down the movements over the last 90 days, this pattern becomes self-evident. Multiple independent indexes all changed their inclusion criteria to accommodate the SpaceX IPO. And their changes specifically loosed the guardrails that were put in place to protect retail investors from the information asymmetry between themselves and institutional investors.

Let’s understand how in more detail.

How Were the Index Guardrails Dismantled to Allow SpaceX-like Low-Float Listings?

Credit where credit is due: the passive investment industry spent the last decade building some good investor protections from predatory private listings. These protections were engineered after specific corporate failures left index investors holding illiquid, un-voted shares. The guardrails relied on four structural pillars:

Seasoning Windows: The S&P Composite 1500 required an IPO to complete 12 months of active public trading before index entry, allowing initial lockups to expire and public financial data to surface.

Float Minimums: Standard benchmarks required at least 10% of a company’s total shares to be available for public trading, preventing tiny allocations from causing massive price volatility.

Profitability Screens: Inductees were required to show positive GAAP net income over their most recent four quarters, ensuring index entry was backed by real accounting profits rather than market hype.

Voting Floor Rights: Following Snap’s zero-vote share offering in 2017, FTSE Russell barred companies unless public shareholders held at least 5% of total voting power, while S&P closed the S&P 500 to new multi-class structures.

These protections were systematically broken down between February and June of this year to accommodate Elon’s newest rug pull:

Under the old rules, a company selling only 4% of its shares to the public was automatically disqualified for failing the 10% float threshold.

Under the new rules, if that 4% slice is worth billions of dollars, the percentage minimum is waived entirely. At a $1.77 trillion valuation, SpaceX’s tiny 4.15% public float translates to a $75 billion offering — a dollar figure larger than the total market cap of most companies in the index.

(The float constraints are more important than you’d realize. If only a small percentage a company is available, then its price will fluctuate much more violently, which can adversely impact investors. This way Elon and his buddies get to keep all the control, while still forcing indexes to buy their inflated valuations).

A more detailed analysis is given below:

As you can see here, multiple indexes clearly rewrote their rulebooks to accommodate these changes, all to make it easier for them to let them cash out on that sweet 401-k demand. The scalpers that will price this demand to dump stuff will win. Elon’s cronies will win bigly. Even the index managers will win since they make money irrespective. The only one that loses is the regular investor that thought that someone would look out for them. That’s what we get for being poor and focusing on actually contributing to society instead of trying to weasel around and steal value from every nook and cranny of the system.

Luckily, people have started speaking out against this, sparking a public confrontation that forced the S&P 500 committee to draw a hard line on its core index family. While this is a win, I think many people overestimate what this actually means (I heard from more than a few people that this was all we needed and everything would sort it itself out now). Let’s understand why this isn’t true.

Does the S&P 500 Rejection of SpaceX Protect You?

The S&P 500 committee’s June 4 decision to reject the “MegaCap” rule changes creates a dangerous illusion of systemic safety. The committee’s proposal on April 30 had suggested halving the 12-month waiting period, waiving the 10% public float minimum, and dropping the positive GAAP net income screen for exceptionally large companies. While public opposition forced the committee to declare that rule exceptions “should not be granted solely based on market capitalization,” this firewall only applies to the S&P 500 index family itself.

This is a problem because an asset entering through the newly opened side doors of total-market, Nasdaq, and Russell indexes begins accumulating the exact milestones required to clear the front gate later. Over a 12-month seasoning window, an unlisted mega-cap stock builds up trading history, converts insider shares into float as lockups expire, and establishes passive institutional ownership patterns.

Furthermore (and this is important), S&P’s own June 4 document authorized these low-float alternatives for its Total Market, Completion, and Dow Jones U.S. Total Stock Market benchmarks. Entry into these foundational total-market products automatically feeds into specialized sub-indexes:

Total-market entrants become eligible for immediate inclusion in derived size, style, sector, factor, and sustainability benchmarks.

Investors who choose a supposedly safe “Growth” or “ESG” index product absorb the low-float asset layout without realizing they have bypassed the core S&P 500 profit screens.

The exposure propagates into target-date retirement vehicles that use total-market building blocks as their primary equity holdings.

So the S&P ruling doesn’t even fully extend across their own families. Safety Theatre at its finest.

And if we let this pass, then things are only going to get worse. Silicon Valley has rug-pulled retail investors through overpriced IPOs based on misinformation and hype for a while now; but at least investors could choose to not engage. If these index changes are allowed to stand, it will create a strong pipeline where retail investors will permanently have to bail out the so-called smart money. And that lineup already looks promising:

Anthropic filed its confidential draft S-1 on June 1, following a $65 billion funding round that established a $965 billion valuation backed by a $47 billion annualized revenue run-rate (wait till we dissect this can of worms, there is a LOT wrong here).

OpenAI finalized its own confidential SEC paperwork on June 8 at a valuation nearing $852 billion, completely omitting public financials, share distributions, or corporate voting structures.

Fun times ahead. But can we do anything about this?

As always, you have more power than you think.

What Can YOU Do to Block Forced Index Entry?

Contrary to what some wimps peddle online, people hold enough leverage to make things happen. Reversing this automated robbery requires formal, documented intervention through structured fiduciary and regulatory channels. The following list might seem overwhelming, but the key is to organize as a collective, pick 2–3 sides that best suit us, and focus on that. If everyone focuses on their battle, the collective

First, you can protect yourself better by executing three steps:

Audit Fund Benchmarks: Locate the “seeks to track” statement on your index fund profile pages to identify your direct exposure. If your portfolio holds products tracking the CRSP U.S. Total Market Index, the FTSE Global All Cap, the Nasdaq-100, or S&P total-market benchmarks, your money is exposed.

Submit a Formal ERISA Prudence Query: Route a written request to your employer’s 401(k) plan investment committee through Human Resources, requiring a formal response on the record. This places a binding duty of review on individuals who face personal legal liability under ERISA Section 404(a), which mandates care, skill, prudence, and diligence in monitoring plan options. Most importantly, this will force the issue onto the plan’s fiduciary record.

Demand Restricted Equity Alternatives: Use your plan’s feedback loop to demand at least one broad equity selection that is structurally insulated from immediate low-float IPO entry — such as a standard S&P 500 fund, a profitability-screened index, an equal-weight benchmark, or a self-directed brokerage window.

Not sure what to send? Here’s something nice and easy drafted by Irys — “I am a participant in [plan name]. I am writing to ask whether the plan’s investment committee has reviewed the 2026 IPO fast-entry and low-float methodology changes adopted by Nasdaq (effective May 1), FTSE Russell (May 26), CRSP/Morningstar (April 27), and S&P Dow Jones total-market indexes (June 8), as well as MSCI’s existing large-IPO early-inclusion process, and whether the committee has assessed how these changes affect the plan’s index funds and target-date funds-including exposure to newly public, low-float, controlled companies such as SpaceX. I request a written response. Under ERISA section 404(a) and in light of the Department of Labor’s March 30, 2026 proposed rule on designated investment alternatives, I believe benchmark methodology, valuation, liquidity, and complexity are appropriate subjects for the committee’s documented review.”

(While the bar for ERISA litigation is high and plan fiduciaries are generally afforded broad discretion in selecting diversified index funds, these formal queries serve a critical strategic purpose. Rather than an immediate trigger for litigation, this documentation acts as a mechanism for transparency — compelling plan sponsors to justify their continued reliance on benchmarks that have systematically dismantled their own governance screens. By forcing this issue onto the official record, you ensure that the decision to expose retirement savings to low-float, high-volatility listings is a conscious, documented choice rather than an automated oversight. Historically, it is this type of granular scrutiny that forces corporate consultants and fiduciary insurers to re-evaluate structural risks, eventually steering capital away from exposed benchmarks to avoid the long-term threat of ‘failure to monitor’ claims).

This documentation creates an immediate liability risk for plan sponsors. Historical precedent shows that excessive-fee litigation over the last fifteen years cut 401(k) expenses roughly in half because corporate consultants steered clients away from structural compliance risks. Once “default funds whose benchmarks auto-buy low-float corporate listings” becomes a line item on fiduciary-insurance questionnaires, the spreadsheet merchants will move away from the exposed benchmarks themselves.

You can also escalate this financial pressure by targeting fund boards and index licensing revenue directly. Because index providers earn revenue as basis points on assets benchmarked to their rulebooks, moving capital out of a Russell or CRSP total-market fund and into a standard S&P 500 fund is a good way to immediately punish funds that dissolved their screens. Once again, to really turn the thumb-screws, skip the IR departments and write directly to a fund’s independent board of trustees, who hold the statutory authority to approve index licenses and tracking policies.

The most definitive regulatory lever is filing a formal public comment on the Department of Labor (DOL) March 30 proposed rule. Workers can be automatically enrolled into default retirement funds only because federal regulations grant plan sponsors a strict liability safe harbor for utilizing Qualified Default Investment Alternatives (QDIAs). Since federal agencies are legally required to address substantive data within the public register, commenters can dismantle this legal coverage. To trigger this, submit comments demanding that QDIA safe-harbor status be explicitly conditioned on a default fund’s benchmark maintaining rigorous seasoning, minimum public float, and voting-rights screens. Citing the SpaceX listing and the FTSE Russell consultation by name proves that low-float benchmarks carry structural valuation and liquidity risks, forcing corporate lawyers to abandon them to preserve their safe harbor.

For public sector capital, beneficiaries can force state pension systems to act from below. The Comptrollers of New York City and New York State and the CEO of CalPERS have issued public objections calling the SpaceX listing the most management-favorable governance structure ever brought to public markets. State employees and teachers can leverage these admissions to demand that their retirement boards aggressively renegotiate passive investment mandates. Pensions routinely run index-minus-exclusion mandates for firearms or tobacco; beneficiaries can mandate identical exclusions for multi-class, low-float listings (I’d imagine you can also directly point to Grok’s Sexual Deepfakes as a strong reason to not invest into SpaceX, which now owns the AI company). These groups can pull some serious numbers (for eg the American Federation of Teachers (AFT) alone represents 1.7 million members).

Finally, we can also directly confront the regulatory framework governing the indexes themselves. Rather than relying on SEC Rule 14a-8 shareholder proposals — which corporate counsel routinely block under the ‘ordinary business operations’ exclusion — investors should direct their focus toward formal SEC regulatory petitions. By petitioning the SEC to investigate the commercial conflicts of interest between index licensing revenues and investor protection mandates, we can force some action. Morningstar here seems to be the most interesting target: its advisory division issues safety ratings to individual investors while its index division actively waives the screens that protect them.

Then we can attack the root of this extraction: the underlying exchange listing standards. While the SEC and US exchanges have permitted dual-class structures for decades, the SpaceX listing represents an unprecedented compounding of risks. A $1.77 trillion valuation holding ten-to-one insider voting shares and 82% single-person control is concerning on its own. But when combined with waived float minimums and bypassed profitability screens, it creates a systemic vulnerability.

Additionally, maintaining a public ledger that tracks which funds bought on which date, at what price relative to the offer, and the resulting cost-per-household provides standing evidence for future litigation and regulatory enforcement.

Conclusion: What Is the Bottom Line?

There is a common type of cynicism that says everything is rigged, the system is too big, and you cannot do anything about it. That attitude is a cop-out used by cowards to make themselves feel better about their inaction.

The entire index fund machine does not run on Wall Street’s hidden wealth. It runs on your money — the automatic deductions taken out of your paycheck every two weeks. When you start asking tough questions, the people managing that money have to listen.

Throughout history, every good thing that ever happened came about because regular people decided to come together and fight for it. We know this works because we just saw it happen. On June 4, public pressure forced the S&P 500 committee to back down and keep their safety rules in place. Over the last fifteen years, regular people filing complaints cut 401(k) fees in half across the country.

The scale of these giant companies can feel overwhelming, but the way you fight back is simple: pick your battle, find a group to stand with, and stick it out. You do not have to change the whole financial system yourself. You just have to look up your funds, send one written question to your HR department/send messages to indexes, or move your savings to a fund that does not buy into rigged voting structures. Persist with that, and have faith that there are others who have your back.

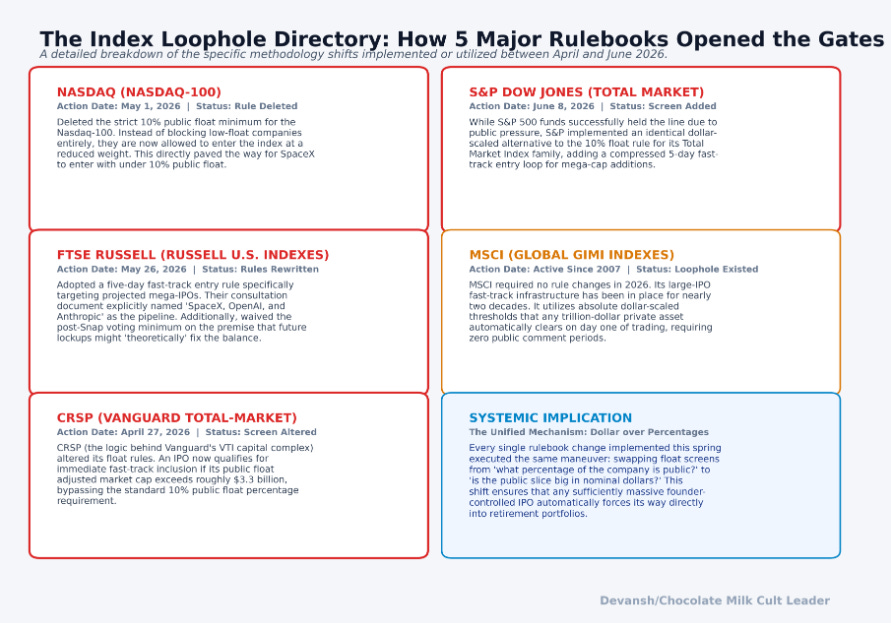

Appendix A: The Five Rulebooks in Detail

Written to be forwarded to a plan committee, legal counsel, or investment consultant.

S&P Dow Jones Indices: Under old rules, the S&P Composite 1500 (including the S&P 500) required a 12-month IPO seasoning window, an investable weight factor (publicly investable share fraction) of at least 0.10, and positive GAAP net income in the most recent quarter and summed over the most recent four. The April 30 consultation proposed halving seasoning to six months, waiving the 0.10 weight factor, and waiving the profitability screen for MegaCap listings. On June 4, S&P rejected these changes for the Composite 1500, stating exceptions should not be granted based solely on market capitalization. However, in the same June 4 document, S&P added a dollar alternative to the 10% float test and a five-business-day fast-track entry clause for its Total Market, Completion, and Dow Jones U.S. Total Stock Market indexes, implemented June 8. Entrants in these total-market families may become eligible for derived size, sector, style, factor, and sustainability indexes.

Nasdaq (Nasdaq-100): Old rules required a 10% minimum free float, and new listings waited for scheduled reconstitutions. A February consultation proposed fast entry for new listings with full market capitalization within the top 40 constituents, replacing the float minimum with a weight cap of five times free float. Nasdaq finalized the rule effective May 1, adopting fast entry after the 15th trading day based on evaluation on the 7th trading day, and softening the weight cap to three times free float. A company with 5% float that was previously excluded now enters at reduced weight. Reuters reported March 10 that SpaceX made early Nasdaq-100 inclusion a necessary condition for its listing venue; Nasdaq states the rule was not written specifically for SpaceX.

FTSE Russell (Russell U.S. Indexes): Old rules added IPOs during scheduled quarterly reconstitutions and required a minimum 5% free float alongside a minimum 5% of total voting rights in public hands. On May 26, FTSE Russell adopted a fast-entry rule for IPOs with investable market capitalization above the Russell Top 500 breakpoint, forcing index addition after the close of the fifth trading day based on first-day closing prices. The platform’s February consultation explicitly named projected 2026 IPO targets motivating the shift: “SpaceX, OpenAI, Anthropic.” The final rule waives the 5% float and voting floors if future lockup expirations are expected to cure the deficit within 12 months, and adds the stock all at once rather than staging entry. Russell U.S. indexes benchmark $11.6 trillion, with $2.7 trillion in passive mandates.

CRSP / Morningstar Indexes: Old rules required a strict 10% public float for fast-track IPO entries. Effective April 27, CRSP altered its float screen to allow fast-track inclusion if an IPO has a 10% float or if its float-adjusted market capitalization is at least one-half basis point of the index-eligible universe, which is roughly $3.3 billion. This index suite benchmarks more than $3 trillion, including Vanguard’s total-market complex. CRSP is transitioning its governance to Morningstar Indexes on July 1.

MSCI (Global Investable Market Indexes): MSCI made no rule changes in 2026 because its Global Investable Market Index methodology has contained early inclusion loops for large IPOs since 2007. To qualify for early entry, an IPO must clear length-of-trading and liquidity screens, hit a full market capitalization of 1.8 times the interim size segment cutoff, and hit a free-float-adjusted market cap of 1.8 times half that cutoff. These dollar-scaled rules mean a trillion-dollar company with a low percentage float clears the hurdle automatically. On June 8, MSCI confirmed this process applies to SpaceX, with inclusion announced between the first and third trading day and made effective after the close of the tenth.

Appendix B: The SpaceX S-1 Balance Sheet Dissection

All figures are compiled directly from the June 3 amended S-1 corporate filing.

The Offering Layout: The company is selling 555,555,555 Class A shares at an expected price of $135 each, raising approximately $75 billion before any underwriter overallotments.

Valuation Multiples: Multiplying $135 by the post-offering Class A and Class B share counts (including outstanding restricted Class B) establishes a total valuation of $1.77 trillion. This multiple is approximately 95 times the company’s full-year 2025 revenue of $18.674 billion.

The Voting Disparity: Class A shares carry one vote per share; insider Class B shares carry ten votes per share. Post-offering, Class B holders retain 88.5% of total voting power, and Elon Musk controls 82.4%. This triggers a “controlled company” status under Nasdaq rules, exempting the firm from standard board governance protections and giving Class B holders the unilateral right to elect a board majority.

Segment Bundling: The corporate vehicle reflects a February 2026 transaction where SpaceX acquired xAI, following xAI’s 2025 acquisition of X. Financial statements are recast retroactively under common control to bundle four distinct operations: Starlink, launch/space, X, and xAI.

Consolidated Loss Metrics: In full-year 2025, the company posted revenue of $18.674 billion, an operating loss of $2.589 billion, and a final net loss attributable to common shareholders of $4.937 billion, alongside adjusted EBITDA of $6.584 billion. For the first quarter of 2026, the company recorded revenue of $4.694 billion, an operating loss of $1.943 billion, and a net loss of $4.947 billion.

Segment Operational Realities: The Connectivity segment (primarily Starlink) generated $11.387 billion of 2025 revenue, $4.423 billion of operating income, and $7.168 billion of adjusted EBITDA. The Space segment posted $4.086 billion of revenue and an operating loss of $657 million. The AI division logged $12.727 billion in capital expenditures for 2025 and accelerated to $7.723 billion in capital expenditures for the first quarter of 2026 alone — a run rate that annualizes to more than the entire company’s consolidated revenue.

Treasury Crypto Holdings: As of March 31, 2026, the corporate treasury held 18,712 bitcoin with a reported fair value of $1.293 billion, down from a fair value of $1.637 billion at year-end 2025.

Appendix C: Academic Literature + Links for Your Research

Compiled academic literature detailing the transaction drag imposed by automated, schedule-driven rebalancing trades. These were cited and linked in-line, but I’m also inclufing them so you have an easier time sourcing the research/claims.

Harvey, Mazzoleni, and Melone (“The Unintended Consequences of Rebalancing”): Documents that predictable, mandatory institutional index rebalancing trades cost investors roughly $16 billion per year in execution penalties. This extraction transfers approximately $200 per year out of every indexed U.S. household.

Sammon and Shim (“Index Rebalancing and Stock Market Composition”): Evaluates rebalancing execution data in the Journal of Financial Economics and finds that predictable index rebalancing trades impose a structural drag of 46 to 69 basis points per year on passive index fund returns. The paper demonstrates that capitalization-weighted index math mechanically forces funds to purchase shares at peak run-ups and high-volume corporate issuances.

Arnott, Brightman, Kalesnik, and Wu (“The Avoidable Costs of Index Rebalancing”): Tracks the performance delta of discretionary adjustments and finds that companies deleted from the S&P 500 outperform the mandated new stock additions by an average of 22% over the 12 months following index rebalancing. This proves that accelerated entry mechanisms force passive capital to buy assets when they are overvalued.

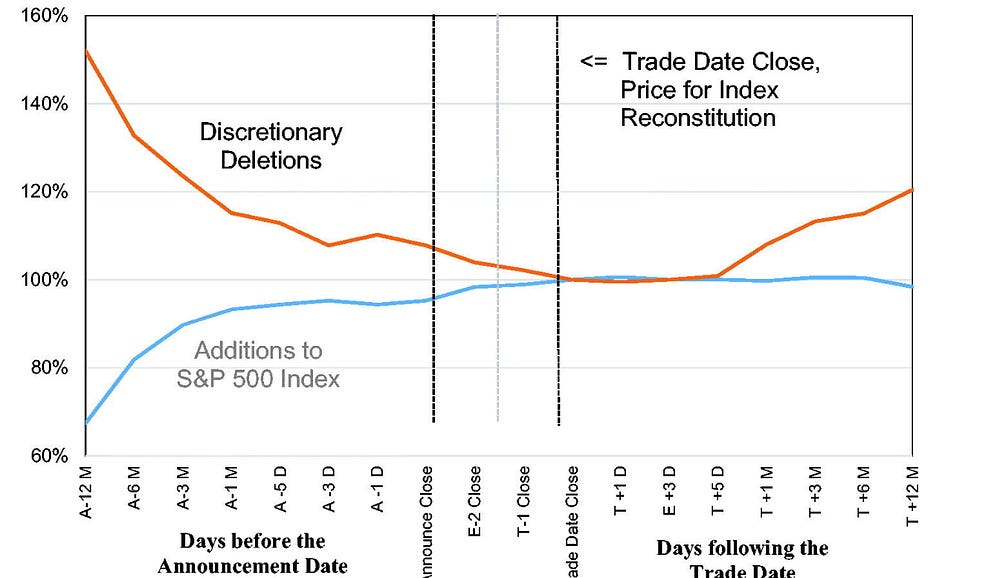

Greenwood and Sammon (“The Disappearing Index Effect”): Analyzes inclusion day price behavior and details how the historic price pop on the day a stock joins the S&P 500 fell from an average of 7.4% in the 1990s to just 0.3% over the last ten years. The data shows that forced buying has not become cheaper, but has shifted chronologically: algorithmic traders chart the published index methodologies weeks in advance, accumulate the target stock early, and sell it to index funds at prices that already reflect the automated demand.

Sources:

S&P Dow Jones Indices, June 4 results announcement and April 30 MegaCap consultation.

Nasdaq, February 2026 consultation, summary of responses and conclusion, and methodology update explanation.

Reuters, March 10 report on SpaceX seeking early Nasdaq-100 inclusion.

FTSE Russell, IPO fast-entry consultation, May 26 press release, and technical notice.

CRSP, float-shares investability screen notice and methodology guide.

MSCI, SpaceX IPO update, Megacap IPOs explainer, GIMI methodology, and Corporate Events methodology.

SpaceX, June 3 amended S-1.

Anthropic, confidential draft S-1 announcement and Series H announcement.

AP, OpenAI confidential SEC paperwork report; CBS News, OpenAI confidential IPO statement.

Vanguard, VTI benchmark and VT benchmark; Invesco, QQQ benchmark.

AFT, May 6 letter to the SEC; NYC Comptroller, NYS Comptroller, and CalPERS, letter to SpaceX.

U.S. Department of Labor, March 30 proposed rule fact sheet.

Thank you for being here, and I hope you have a wonderful day,

Dev <3

If you liked this article and wish to share it, please refer to the following guidelines.

That is it for this piece. I appreciate your time. As always, if you’re interested in working with me or checking out my other work, my links will be at the end of this email/post. And if you found value in this write-up, I would appreciate you sharing it with more people. It is word-of-mouth referrals like yours that help me grow. The best way to share testimonials is to share articles and tag me in your post so I can see/share it.

Reach out to me

Use the links below to check out my other content, learn more about tutoring, reach out to me about projects, or just to say hi.

Small Snippets about Tech, AI and Machine Learning over here

AI Newsletter- https://artificialintelligencemadesimple.substack.com/

My grandma’s favorite Tech Newsletter- https://codinginterviewsmadesimple.substack.com/

My (imaginary) sister’s favorite MLOps Podcast-

Check out my other articles on Medium. :

https://machine-learning-made-simple.medium.com/

My YouTube: https://www.youtube.com/@ChocolateMilkCultLeader/

Reach out to me on LinkedIn. Let’s connect: https://www.linkedin.com/in/devansh-devansh-516004168/

My Instagram: https://www.instagram.com/iseethings404/

My Twitter: https://twitter.com/Machine01776819

IYH Essay for essay the best value on substack. FWIW when I analyzed in 2010 the Flash Crash, and talked to HFT guys, and realized retirement funds were being fleeced by exactly the same predictable on-this-date-we-do-X engineered liquidity arbitrage, I was told the retirement funds guys deserved it for being so dumb and predictable. It was not seen as affecting millions of Americans, but a game of slow-witted dumb fund managers vs hypersmart algo guys.

FWIW Credit Suisse in 2015 actually published several datasheets showing the exact 'commands' in Dark Pools and elsewhere the 'commands' used by HFT for this algo market manipulations. All out in the open, this is how shameless this is.

Space x literally spoke to Nasdaq about index inclusion as a condition for listing in there. So this isn't just the indexes operating like this.

Also the IPO is oversubscribed because of the forced liquidity. Refer to DBs comment on the same.