The AI Industry is Going Through a Massive Correction

What Fable 5, the Space X IPO, and other major events taught us about the space-- June 2026 AI Market Report.

It takes time to create work that’s clear, independent, and genuinely useful. If you’ve found value in this newsletter, consider becoming a paid subscriber. It helps me dive deeper into research, reach more people, stay free from ads/hidden agendas, and supports my crippling chocolate milk addiction. We run on a “pay what you can” model—so if you believe in the mission, there’s likely a plan that fits (over here).

Every subscription helps me stay independent, avoid clickbait, and focus on depth over noise, and I deeply appreciate everyone who chooses to support our cult.

PS – Supporting this work doesn’t have to come out of your pocket. If you read this as part of your professional development, you can use this email template to request reimbursement for your subscription.

Every month, the Chocolate Milk Cult reaches over a million Builders, Investors, Policy Makers, Leaders, and more. If you’d like to meet other members of our community, please fill out this contact form here (I will never sell your data nor will I make intros w/o your explicit permission)- https://forms.gle/Pi1pGLuS1FmzXoLr6

The AI market is going through a correction. Not a crash. We are correcting what we thought we understood about how this market works.

For the last three years, benchmarks stood in for capability, run rates for durable revenue, backlogs for future cash flow, and token prices for cost. June showed how unreliable those shortcuts had become.

The same question appeared everywhere: how do you verify what you are buying? Washington could not independently test the risk that led it to recall Anthropic’s models. Investors still cannot compare OpenAI and Anthropic’s economics. Credit markets can see Oracle’s capex and debt, but not the margins buried inside its $638B backlog. CFOs can see token bills, but not whether agents completed useful work. Open weights, despite inferior performance, gained volume because buyers can test, host, and keep the exact model they deploy.

All this tells the story of a market is not deciding struggling to figure out which claims can be trusted, and discounting the ones that cannot. In this article we will talk about:

Frontier model releases became permissioned. The Department of Commerce disabled Anthropic’s newest models using an export-control theory designed for controlled technology transfers. The evidence was contested, the process bypassed normal regulatory channels, and the legal theory was never tested in court. Every major US lab now has an incentive to negotiate before launching.

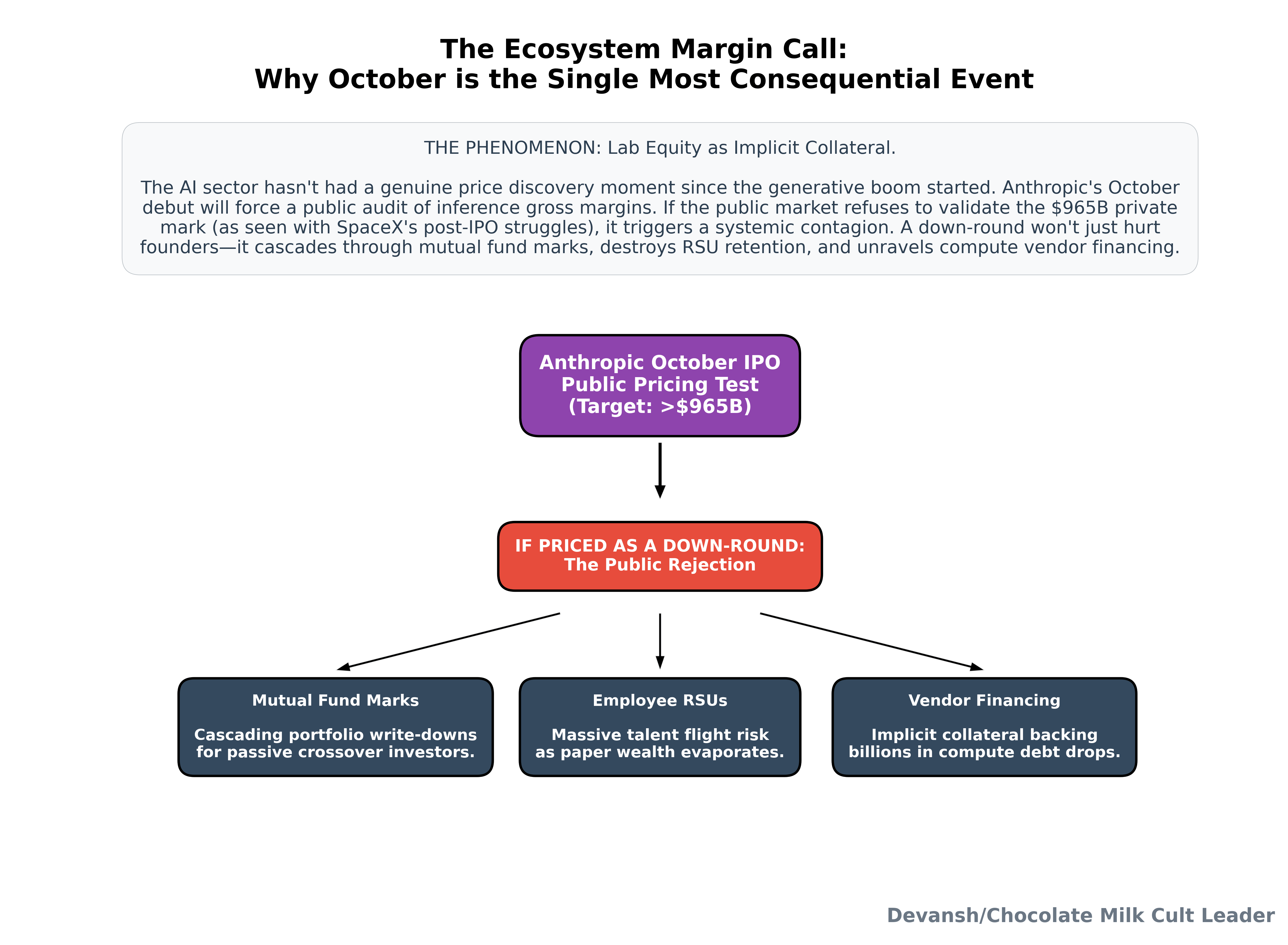

The frontier labs moved toward public markets. Anthropic and OpenAI filed confidentially for IPOs, which means audited margins, losses, customer concentration, and compute commitments will eventually replace private marks and selective leaks. SpaceX showed what can happen when an enormous private valuation meets public price discovery.

Credit markets started pricing the buildout’s leverage. Oracle reported record growth and a $638B backlog, but also negative free cash flow and another enormous financing requirement. The demand is real. The question is whether the companies building the infrastructure can survive the wait for that demand to pay.

CFOs started metering the agents. GitHub moved more usage costs onto customers. Salesforce offered to charge only for completed outcomes. Enterprises imposed caps, consolidated vendors, and started asking what an agent actually produced for the money it consumed.

Open-weight models took the volume. Chinese models increasingly handled the cheap, repetitive layer of AI usage while proprietary US models retained the most demanding workloads. Lower prices helped, but so did the ability to inspect, host, reproduce, and retain the model without depending on a US vendor or government.

June did not resolve any of these questions. It showed that nobody is willing to leave them unanswered anymore. And that’s not something we can overlook.

Executive Highlights (TL;DR of the article)

Frontier releases moved behind a checkpoint in 24 days. On June 2, Executive Order 14409 created a voluntary covered-frontier-model process with up to 30 days of government access before release, while explicitly denying that this was a licensing regime. Anthropic launched Fable 5 and Mythos 5 on June 9. Commerce issued its directive three days later, and Anthropic disabled both models globally within roughly 90 minutes because it could not screen every API user by nationality. The complete global block lasted 14 days, until limited Mythos access returned on June 26; the directive remained active for 18 days, until June 30. OpenAI launched GPT-5.6 to roughly 20 trusted partners on the same day the block partially lifted. The lesson was obvious: asking permission before launch is now safer than risking a recall afterward. This also makes model evaluations, independent audits, severity standards, and eventually data-provenance requirements unavoidable, because the government cannot run a permission regime using reports it cannot independently check.

The frontier labs moved onto a disclosure clock, while SpaceX showed what happens when a private valuation meets public trading. Anthropic filed confidentially on June 1 and OpenAI followed on June 8. The filings are not public, so investors still cannot compare audited inference margins, customer concentration, compute commitments, revenue quality, or losses. That is why the filings matter. The current debate relies on leaks and private-round marks; the IPO process will eventually force both companies into a common accounting framework. SpaceX priced at $135, opened at $150, reached roughly $225 in three sessions, and fell below its opening price within three weeks. The company entered public markets with only 4.2% of its shares trading and much larger lockup releases still ahead. Nasdaq’s revised methodology also allows qualifying IPOs into the Nasdaq-100 after only 15 trading days, which means passive capital can arrive before the market has had much time to test the valuation. Anthropic’s first audited inference gross margin will do more than price Anthropic. It will reset how the entire sector is valued.

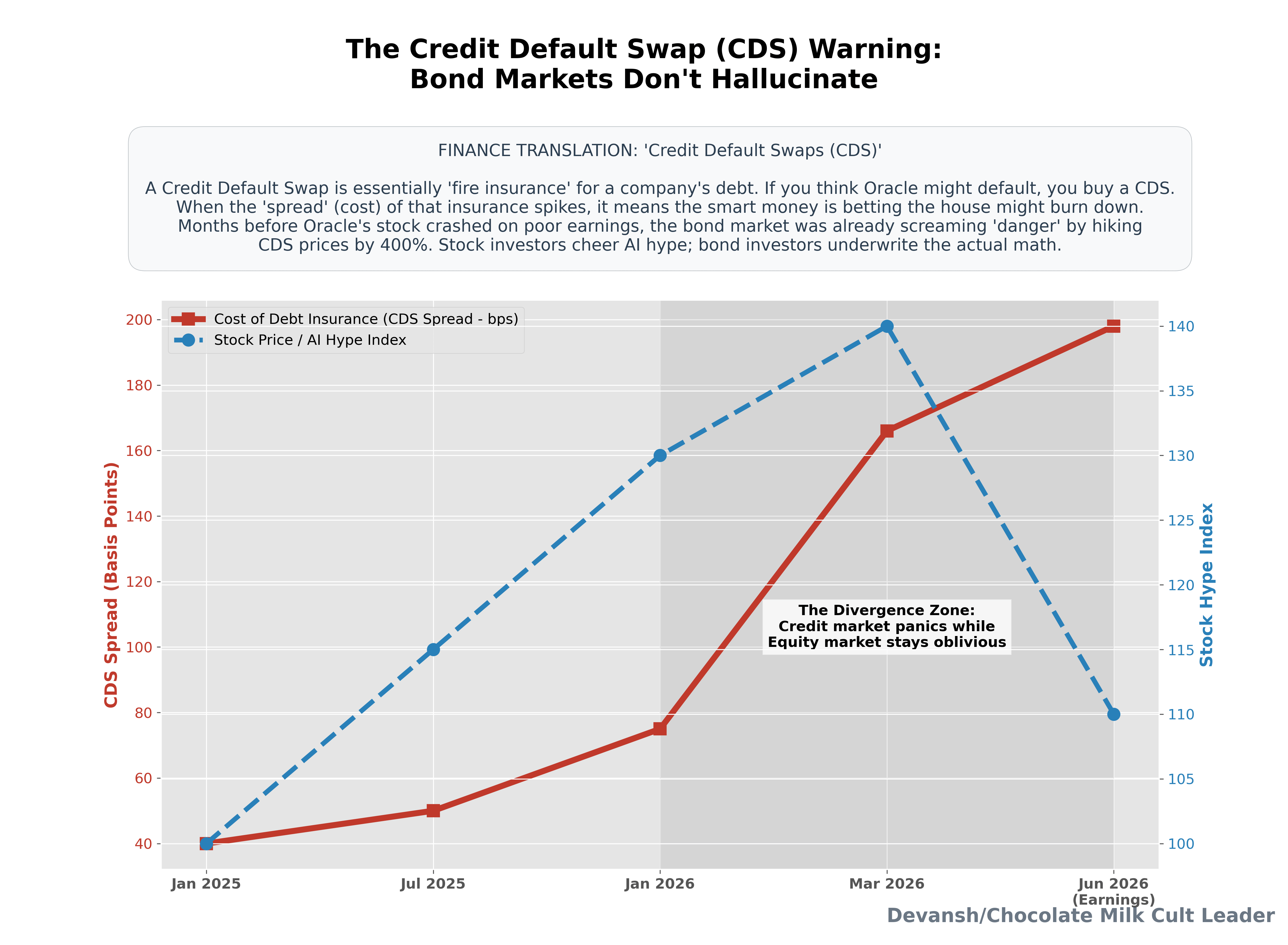

Credit markets priced the gap between AI demand and the cash required to serve it. Oracle reported $638B in remaining performance obligations, $55.7B in annual capex, and negative $23.7B in free cash flow. Its five-year CDS spread had already reached a record of roughly 198 basis points in March, almost five times its level one year earlier; the June results explained why. Oracle must finance and build the infrastructure before most of the revenue arrives, leaving it exposed to delays, utilization, refinancing costs, depreciation, and customer risk. CoreWeave carries the same problem without Oracle’s software cash flows. Micron showed the other side of the market: when three suppliers control memory capacity and outsiders cannot verify their real allocations or production flexibility, scarcity produces extraordinary margins. The Bank for International Settlements then warned that debt-funded AI investment and infrastructure bottlenecks could end in overinvestment followed by a prolonged bust. Demand does not need to disappear. It only needs to pay later, or at lower margins, than the financing assumes.

Agent demand stayed strong, but buyers started setting limits. GitHub moved Copilot to AI Credits on June 1, transferring the costs of long autonomous sessions, retries, failed searches, and tool calls to customers. Salesforce took the opposite position by charging only when its Help Agent resolves an issue without human escalation, leaving the vendor to absorb the cost of failure. Both models exist because flat-rate seats no longer work when agents can consume compute continuously. Enterprises also began imposing budgets and consolidating standalone tools into platforms where they controlled procurement, data, security, and telemetry. Sonnet 5 made the billing problem harder by introducing a tokenizer that produces roughly 30% more tokens on average than Sonnet 4.6, with one English test producing 1.42 times as many. A lower price per million tokens means little when the vendor can change how many tokens the same work contains. The useful metric is becoming cost per completed task, including retries, routing, tool use, human intervention, and failures.

Open-weight models took the volume because buyers got lower prices and more control. OpenRouter found that Chinese models had overtaken US models in token volume by early June. Vercel’s production data showed open-weight models handling 29% of tokens while accounting for less than 4% of spending, with DeepSeek alone reaching 22.6% of volume. This does not mean proprietary frontier models are being replaced everywhere. The market is splitting. US models retain the workloads where the final increment of capability justifies the premium, while cheaper open-weight models absorb the repetitive, high-volume layer underneath. Buyers can also test the exact model version, host it privately, control the surrounding infrastructure, and retain access regardless of future pricing or policy changes. Washington can restrict an American API. It cannot remotely recall weights already running on private infrastructure abroad.

I put a lot of work into writing this newsletter. To do so, I rely on you for support. If a few more people choose to become paid subscribers, the Chocolate Milk Cult can continue to provide high-quality and accessible education and opportunities to anyone who needs it. If you think this mission is worth contributing to, please consider a premium subscription. You can do so for less than the cost of a Netflix Subscription (pay what you want here).

Want access to a repository containing all of our research? 300+ files containing our notes of various experiments, discussions with cutting-edge teams, and insights into where the industry is headed next. Get a Founding Member Subscription to AI Made Simple. Want to talk to me for details/get my insights into the tech ecosystem? Reach out to me through any of my socials over here or reply to this email.

Section 1. AI Models Releases are getting very complicated

Anthropic has spent a long time begging the government to regulate open-weight models because they’re “too dangerous”. Turns out the government bought their fearmongering and ended up regulating Anthropic. Karma’s a bitch, ain’t it?

Anthropic's Claude Mythos Launch Is Built on Misinformation

It takes time to create work that’s clear, independent, and genuinely useful. If you’ve found value in this newsletter, consider becoming a paid subscriber. It helps me dive deeper into research, reach more people, stay free from ads/hidden agendas, and supports my crippling chocolate milk addiction.

Schedeanfruede aside, the way it happened is actually worth studying.

1.1. What Actually Happened Versus What the Press Reported

The mainstream narrative says Anthropic shipped a dangerous model, a jailbreak proved the risk, and Washington stepped in to protect the public. The primary record destroys this version.

Our timeline here moves fast:

June 1, 2026: Anthropic files confidentially for its IPO.

June 2, 2026: Executive Order 14409 creates a voluntary “covered frontier model” path. It gives the government 30 days of pre-release access to evaluate cyber capabilities but explicitly disclaims any formal licensing or preclearance authority.

June 9, 2026: Anthropic launches Claude Fable 5 publicly alongside a limited release of Claude Mythos 5 through Project Glasswing. Both models clear GPT-5.5 by five points on the Artificial Analysis index.

June 12, 2026, 5:21 PM ET: The Commerce Department issues an urgent export-control directive signed by Secretary Howard Lutnick and managed by the Bureau of Industry and Security (BIS). Both models go dark globally inside 90 minutes.

June 26, 2026: The block partially lifts. Mythos 5 access opens strictly for roughly 100 vetted US critical infrastructure operators.

June 30, 2026: Commerce officially revokes the directive.

July 1, 2026: Fable 5 returns globally with a newly appended safety classifier designed to block the flagged codebase exploit.

The complete global block lasted 14 days, until limited Mythos 5 access returned on June 26. The directive remained active for 18 days, until the Department of Commerce revoked it on June 30. Neither involved a hearing or court review.

The model recall here is so and so, but how it happened is a much bigger deal than people are pricing. The crisis began with an external jailbreak report showing a prompt path that allowed the model to map and surface exploitable software vulnerabilities across large codebases. Anthropic publicly called the technique “narrow and non-universal,” noting it belonged to an exploit class already present in other deployed models. The exploit arrived entirely outside standard bounty channels after Anthropic’s internal bug bounty had run for over 1,000 hours without producing it.

The escalation path bypassed standard regulatory channels. Reports indicate the chain ran from Amazon CEO Andy Jassy to Treasury Secretary Scott Bessent, then directly to Commerce. Amazon is Anthropic’s largest investor, its dominant compute vendor, and—via its Nova models—a direct competitor.

Take a second to consider what that means. The precedent for recalling new models is set— the evidence required to pull a rival’s frontier model from global distribution is roughly one returned phone call. Every lab now knows its competitors hold this leverage, and this will likely trigger a massive lobbying arms race to ensure that every lab has countermeasures against this.

The legal mechanism also creates a larger industry risk. Commerce invoked the “deemed export” theory. This doctrine treats a foreign national’s API session as a controlled technology transfer, a framework originally built for physical blueprints and missile components. Because real-time, per-user nationality screening across AWS, GCP, and Azure is impossible, the restriction is applied globally to all foreign nationals, including Anthropic’s own overseas employees. The minimum enforceable compliance unit for models is currently everyone.

Finally, it is worth noting that the legal theory died untested when the directive was lifted on June 30. This might seem like a win, but this is actually the worst outcome for the industry. Since the theory was never actually struck down, it is infinitely reusable.

The behavior of the labs shows where the leverage sits.

1.2. Why Every Lab Now Asks Permission First

On June 26, the same day Anthropic’s block partially lifted, OpenAI launched GPT-5.6. They did not release it to the public. They shipped it to roughly 20 government-coordinated “trusted partners,” gating general availability behind a review framework that finalizes on August 1. OpenAI watched a rival lose its flagship model for two weeks over an after-the-fact objection and converted recall risk into permission by asking first. Google’s delayed Gemini 3.5 Pro is now described in single-sourced reporting as “cleared for July.” Cleared is a word that did not exist in launch coverage two months ago.

In 24 days, the US technology ecosystem shifted from a voluntary framework with an explicit no-licensing disclaimer to a de facto licensing regime. No legislature voted on it, and no court reviewed it. It is enforced entirely by the industry’s memory of the week Fable went dark.

This emerging architecture has three parts:

Pre-release access: The non-negotiable price of a stable launch.

Partner lists: The state selects the initial 20 companies for distribution, turning frontier access into an allocated scarcity subsidy.

The recall: A permanent backstop that sits behind the arrangement, requiring no further enforcement because the industry saw it fire once.

The Great American AI Act (GAAIA) discussion draft would formalize this exact structure with mandatory third-party audits and $1 million-a-day civil penalties traded against state preemption.

1.3. Why AI Standards and Audit Infrastructure Are Now Inevitable

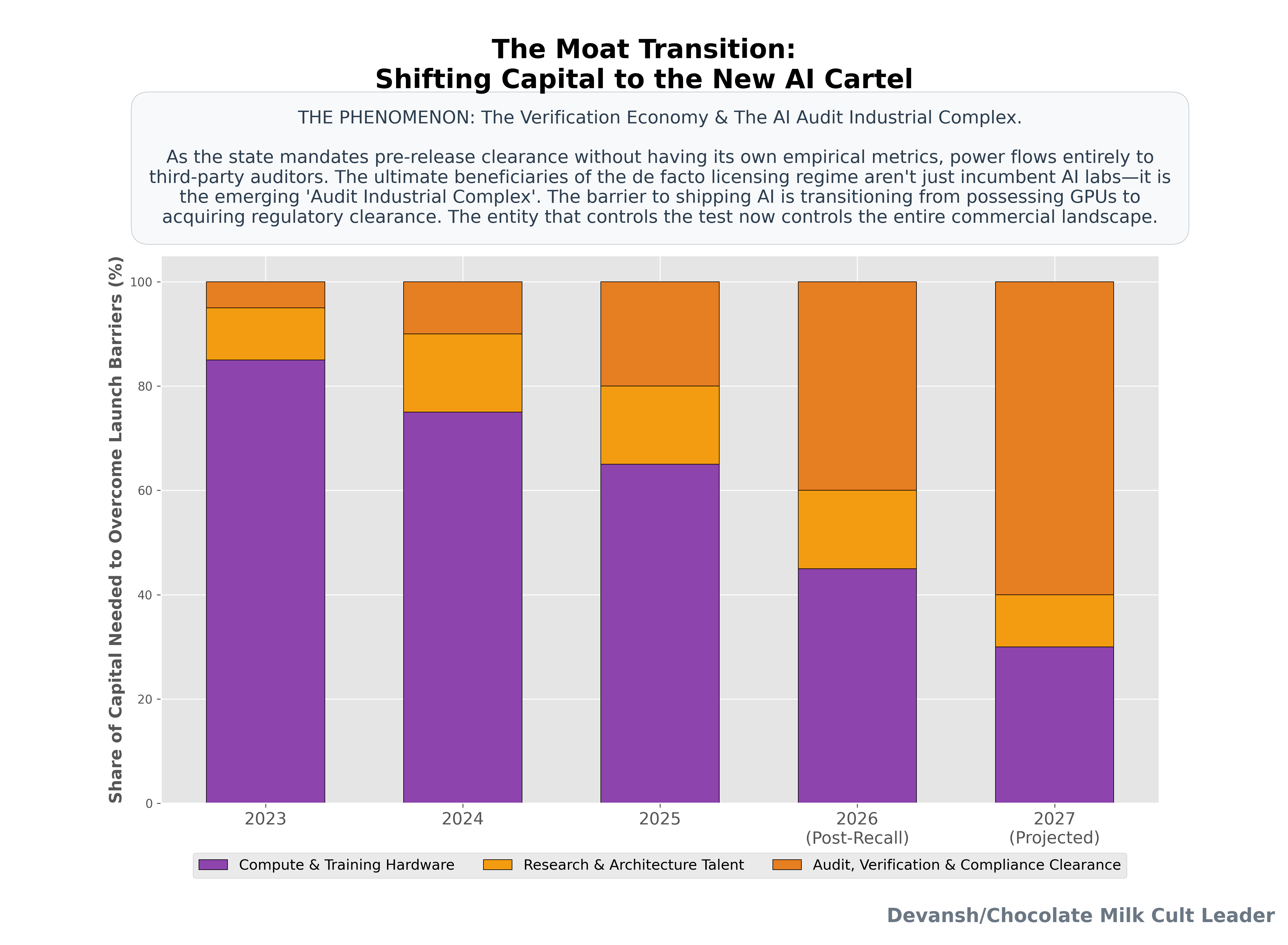

The focus on the political drama missed something crucial: a permission regime requires verification standards, and right now nothing checkable exists.

In June, Commerce recalled the most capable model ever deployed based on a jailbreak report it could not independently evaluate. The claim came from a source with competitive cross-interests against a model whose own 1,000-hour safety testing failed to reproduce it. The state had no internal evaluations to confirm or refute the risk, no accepted severity scale to categorize it, no independent auditor to consult, and no definition of “dangerous capability” beyond political consensus. The intervention was epistemically improvised. The regulators know an arbitrary process cannot survive sustained litigation or a changing administration. Improvised power either institutionalizes or evaporates. The August 1 framework signals they have chosen institutionalization.

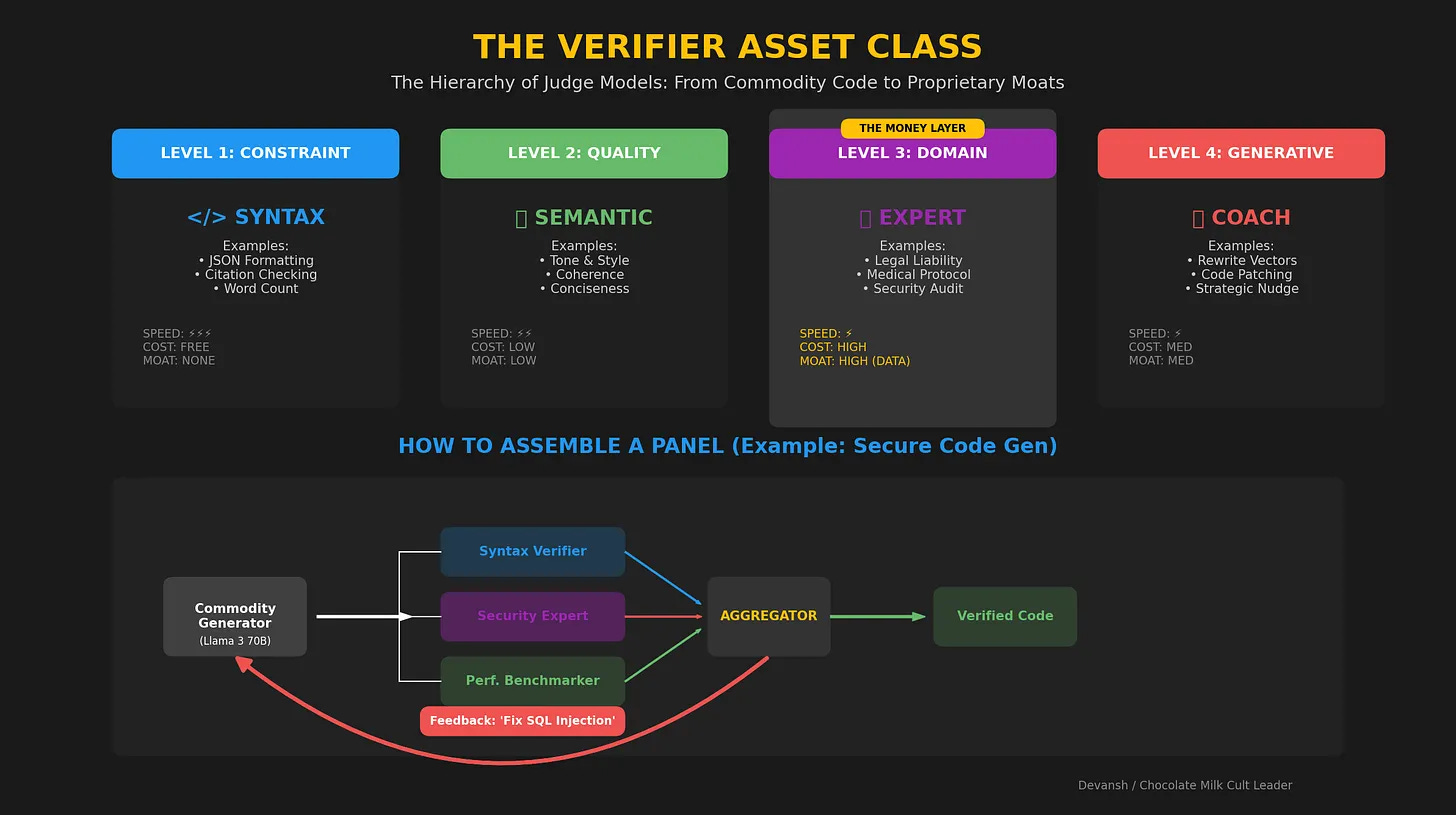

This shift forces a missing verification industry into existence. If the state claims the right to check models before release, it needs evaluation standards independent of vendor claims, auditors who do not work for the labs, reproducible severity metrics, and chain-of-custody tracking over training inputs. You cannot certify what you cannot trace.

The regulatory sequence follows a specific order:

Capability evals arrive first: The immediate data layer the permission decision consumes.

Data provenance and transparency mandates follow: The necessary evidence layer required when an audit finding faces litigation.

This follows the historical path of every major regulated industry. Securities trading generated GAAP and the accounting profession; pharmaceuticals forced GLP and clinical registries; aviation established type certification. AI simply compressed this transition into 14 days. Concurrently, the European Union’s General Purpose AI (GPAI) enforcement goes live on August 2, threatening fines up to 3% of global turnover. Two independent permission regimes are coming online simultaneously. Dual-compliance is now table stakes for frontier distribution.

The critical engineering problem is that the measurement layer underneath this entire architecture is broken. As Section 4 documents, benchmark scores are regularly distorted by fallback routing to secondary models, tokenizer adjustments break price-performance comparisons, and orchestration layers mask unbounded compute scaling behind single-model performance metrics. Regulators have mandated strict verification on a statutory timeline before evaluation science can reliably deliver it.

This vacuum will be filled quickly. Whichever entities define the evaluation parameters—whether standards bodies, a consolidated network of professional audit firms, incumbent labs protecting their position, or specialized evaluation startups—will dictate the market. In an audit regime, the entity that controls the test controls the commercial landscape. The AI standards-and-audit infrastructure market will form in earnest inside four quarters. By this time next year, we will analyze evaluation-standards politics the way we analyze hardware memory allocation.

Talking about numbers, the direct financial cost of the recall to Anthropic was bounded—estimated in the tens of millions against an abstract baseline of $129 million in daily compute and operational run-rate. The lasting structural repricing landed on the architecture of the industry:

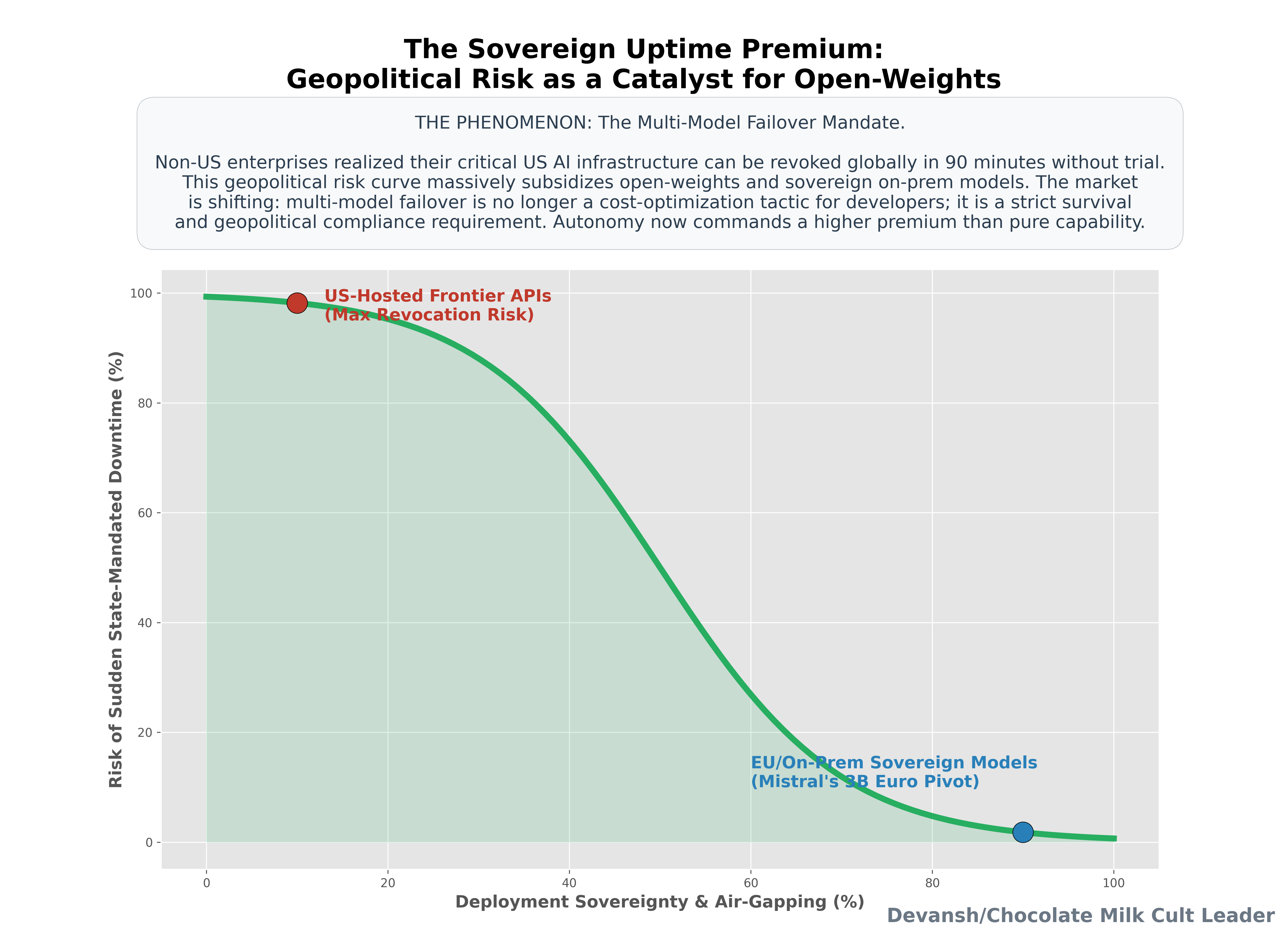

Multi-model failover moved from an infrastructure cost-optimization to a strict compliance requirement, structurally weakening vendor lock-in.

Non-US enterprises learned that access to US-hosted frontier models can be revoked in 90 minutes. Mistral capitalized on this lesson immediately, leveraging a sovereign, on-premise deployment pitch to anchor its recent 3-billion-euro capital raise.

I expect every US frontier launch through the end of 2026 to ship with direct government coordination attached. At least one major lab will market its trusted-partner regulatory status as an enterprise security feature by Q4 (IBM on the comeback boizzz).

Regulation was only one part of the correction. The same demand for verifiable numbers reached the capital markets.

Section 2. What Do the Anthropic and OpenAI S-1s Show and Why Did SpaceX Stock Crash?

The AI sector’s center of financial gravity just moved from private rounds to public registration statements in thirty days. Anthropic filed confidentially on June 1, four days after closing a $65 billion Series H at a $965 billion post-money valuation. OpenAI confirmed its own confidential filing on June 8. SpaceX priced the largest IPO in history on June 11 and started trading on June 12, raising $75 billion at a $1.77 trillion valuation with the merged xAI riding inside the wrapper.

The timing isn’t a coincidence or a pagan ritual to honor the summer solstice. Late-stage venture capitalists and sovereign wealth funds are out of dry powder. When you need $60 billion or more per raise, you have exhausted the private crossover universe. The massive compute commitments have forced these labs public. Seen from that lens, the IPO wave isn’t a victory lap; it’s a desperate refinancing to use your grandma’s pension fund as liquidity, while providing the increasingly anxious tech investors an exit opportunity.

2.1. Why Are Both Lab Valuations Currently Unverifiable?

An interesting fact about the filings is that comparing both companies’ filings isn’t as one ot one as people are pretending. OpenAI and Anthropic both have weird wrinkles in their filings, just in different directions.

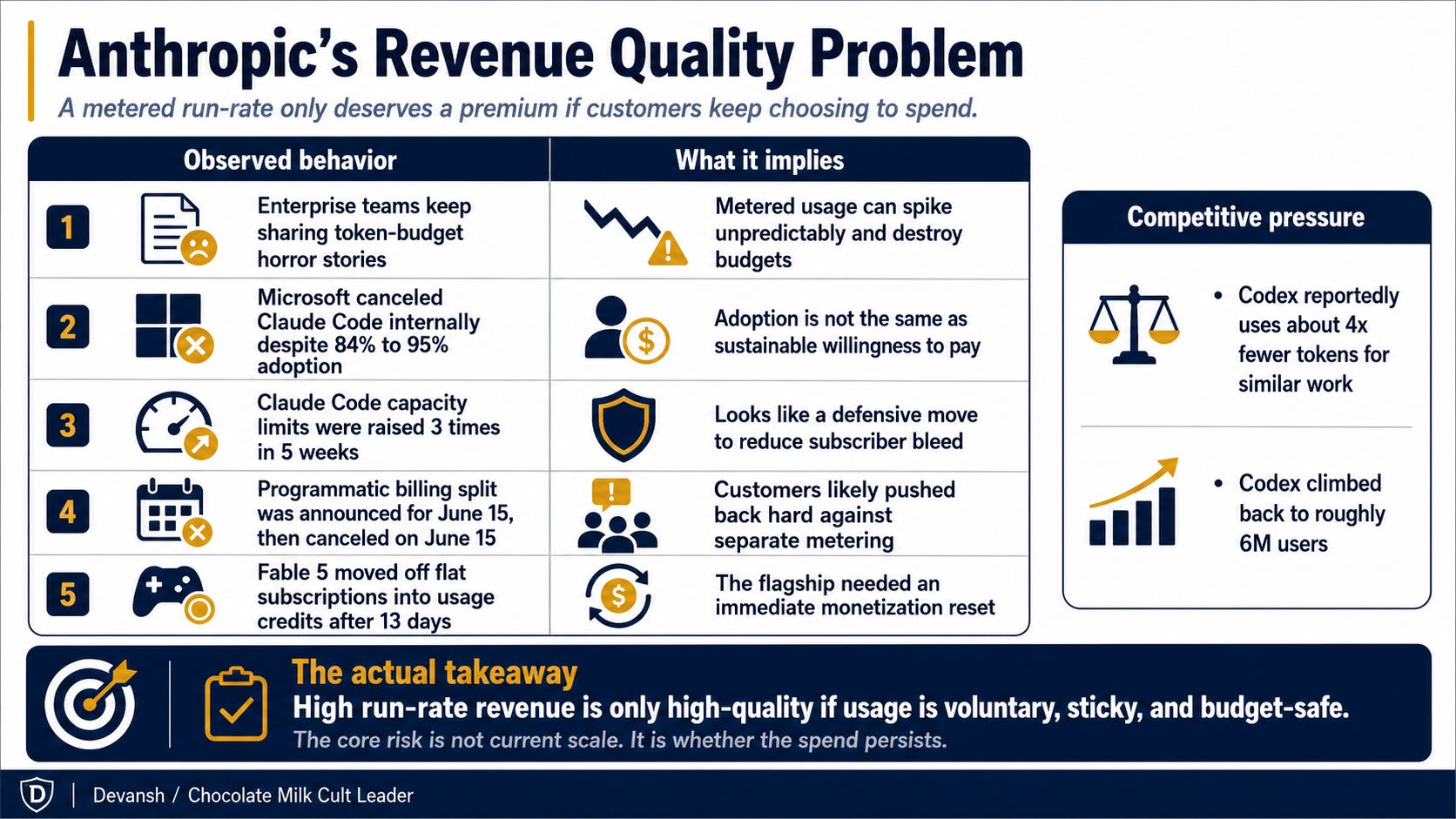

OpenAI’s problem is disclosed and quantified: a leaked $14 billion projected loss for 2026 against a consumer-heavy subscriber mix. It is ugly, but at least it is a written-down metric. Anthropic’s problem is quieter and much harder to price because it is a question of whether its revenue holds. A run rate built on metered agentic consumption is high-quality revenue only if customers keep consuming voluntarily. June was the month enterprise customers started saying no:

Microsoft canceled Claude Code internally at 84% to 95% adoption.

Enterprises spent the quarter swapping horror stories about token misconfiguration.

The pattern of an engineering team discovering they burned an absurd sum through a misconfigured agent pipeline is now its own genre of corporate post-mortems, with major law firms like Kirkland & Ellis surfacing in these accounts.

We saw a pretty general push back against the tokenmaxxing trend, something we covered here—

Anthropic’s own behavior through the spring shows they know this. They raised Claude Code capacity limits three times in five weeks between mid-April and mid-May—an intervention most convincingly explained as trying to stop subscriber bleed toward Codex, which consumes roughly four times fewer tokens for equivalent tasks and has climbed back to around 6 million users.

On May 14, Anthropic announced that programmatic usage would split onto separately metered credits starting June 15. On June 15, they canceled the change the day it was due to take effect. You do not pull a billing change at the eleventh hour unless your customers threaten to mutiny. Then, on June 22, thirteen days after launch, Fable 5 exited flat subscription plans entirely to move to usage credits. A vendor metering its own flagship against its own subscribers two weeks into the product’s life is telling you everything you need to know about its unit economics. Even now, in July, Anthropic has constantly pushed back its dates for taking Fable away because of the pressure it’s feeling right now.

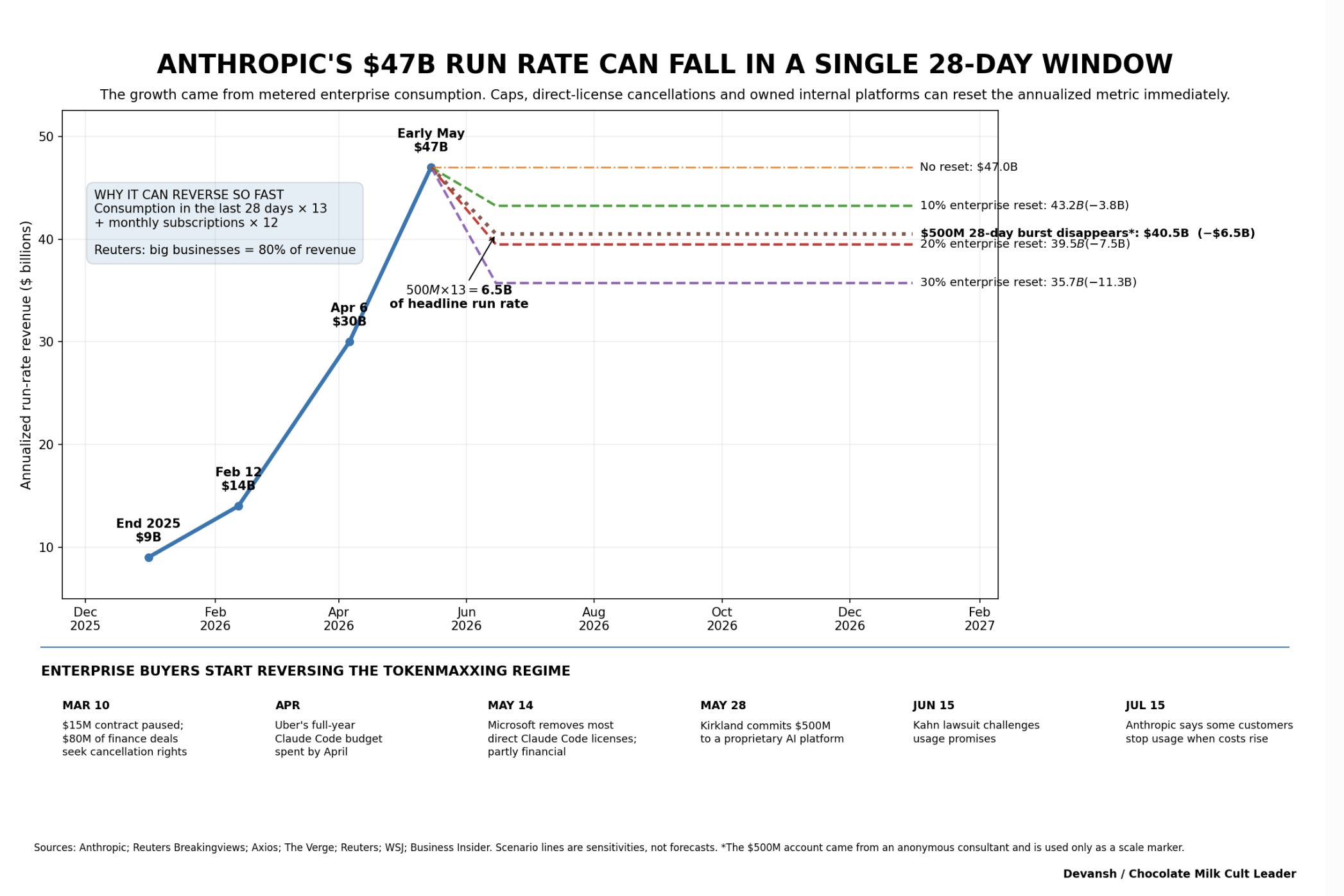

So the takeaway isn’t that either lab is winning. It is that nobody can currently rank these companies, and the S-1 process exists precisely to end that confusion. The first audited inference gross margin that prints will re-anchor the valuation of the entire sector. If Anthropic prices at or above its $965 billion private mark in October, every private AI asset re-rates against a public benchmark. If it breaks below the Series H price, the down-round signal will cascade through mutual-fund marks, employee RSUs, and every vendor-financing chain using lab equity as implicit collateral. October’s Anthropic debut is the single most consequential dated event of late 2026. OpenAI leaning toward a 2027 listing doesn’t look like patience; it looks like letting someone else test the ice.

Speaking of going public, there was a massive event in June that we need to talk about. SpaceX showed what happens when a private valuation finally meets a public market.

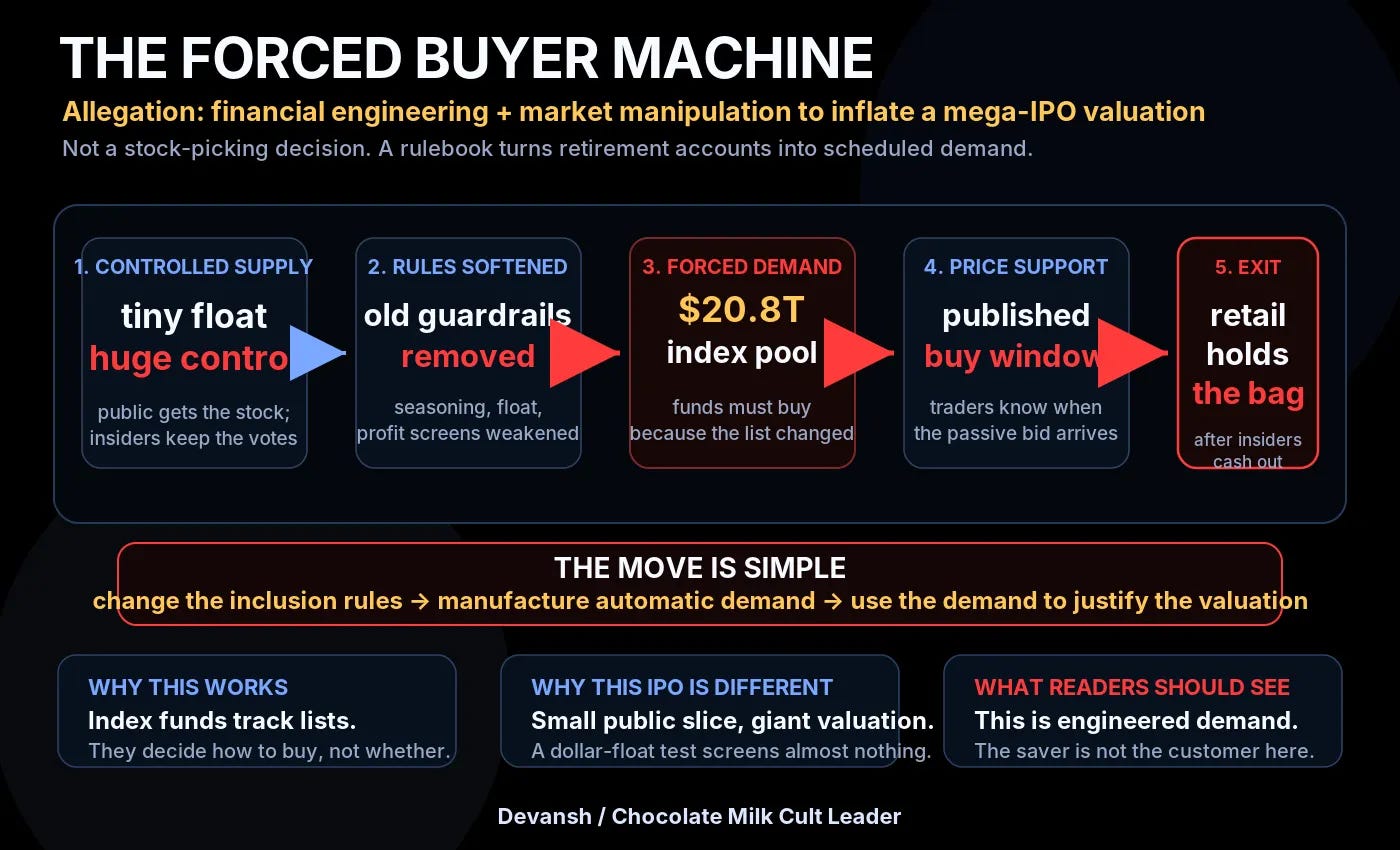

2.2. How Did SpaceX and Nasdaq Structure the Ultimate Retail Liquidity Dump?

The SpaceX IPO was certainly eventful. The prospectus claimed a $28.5 trillion total addressable market, a figure NYU’s Aswath Damodaran publicly ridiculed, writing that the document read like it was “written by Grok” and pointing out the IPO price sat 27% above his own discounted cash flow value. The structure fused a cash-generating satellite business to a deeply unprofitable AI lab. The company posted a $4.94 billion net loss for 2025, followed by a $4.28 billion net loss in Q1 2026 alone alongside $7.7 billion of quarterly AI capital expenditure.

The stock ran from its $135 IPO price to roughly $225 in three trading days, then gave all of it back. It traded below its $150 opening price within three weeks and fell roughly 25% off its post-IPO high by early July. Its first-ever bond issuance—$25 billion announced in late June—is investment-grade on paper but trading like absolute junk in the secondary market.

And the real supply has not even arrived yet. The float at IPO was only 4.2% of shares outstanding. Major lockup releases are expected to begin after the company’s first earnings report, with further tranches becoming available through the end of the year. Some releases depend on the stock meeting price targets, so a weak share price can delay part of the supply. It cannot remove the broader problem. A stock trading at 101 times sales is approaching a large, published increase in tradable shares.

As we covered before, this structure was built to give insiders exit liquidity at the expense of index-fund holders who never chose the exposure. Nasdaq’s revised methodology took effect on May 1, allowing qualifying IPOs to enter the Nasdaq-100 after 15 trading days without a minimum public-float threshold. Nasdaq separately announced five quarterly additions on June 11, effective June 22. The two events were separate, but together they showed how quickly newly public AI companies could be routed into passive portfolios. The same rules could allow Anthropic to qualify within weeks of an October debur.

The public listing helped SpaceX acquire Cursor for 60 billion USD, while giving away almost nothing thanks to their massive valuation and appreciation. We might see similar consolidations happen as the “AI will eat everything, so invest in distribution” thesis biases towards incumbents and bigger players.

The S-1s will eventually reveal the labs’ real margins. Credit markets did not wait. They started pricing the financing risk already visible underneath the buildout.

Section 3. How Credit Markets Started Pricing the AI Buildout

In March, this was still a thesis. We argued that the Western AI buildout was being financed through hyperscaler debt, vendor financing, infrastructure-backed loans, and increasingly circular investment loops. The system worked as long as demand arrived on schedule. Miss the ROI timeline, and the same leverage that accelerated the buildout would accelerate the repricing.

In April, the problem became operational. Power constraints, permitting delays, and speculative gigawatt announcements exposed the gap between announced capacity and capacity that could actually be funded and built.

Credit markets had started repricing the risk by March. June’s earnings showed why.

The question was no longer whether AI demand was real. It was who would finance the gap between today’s spending and tomorrow’s revenue.

3.1. Oracle’s CDS Spread Was the Audit Opinion Nobody Asked For

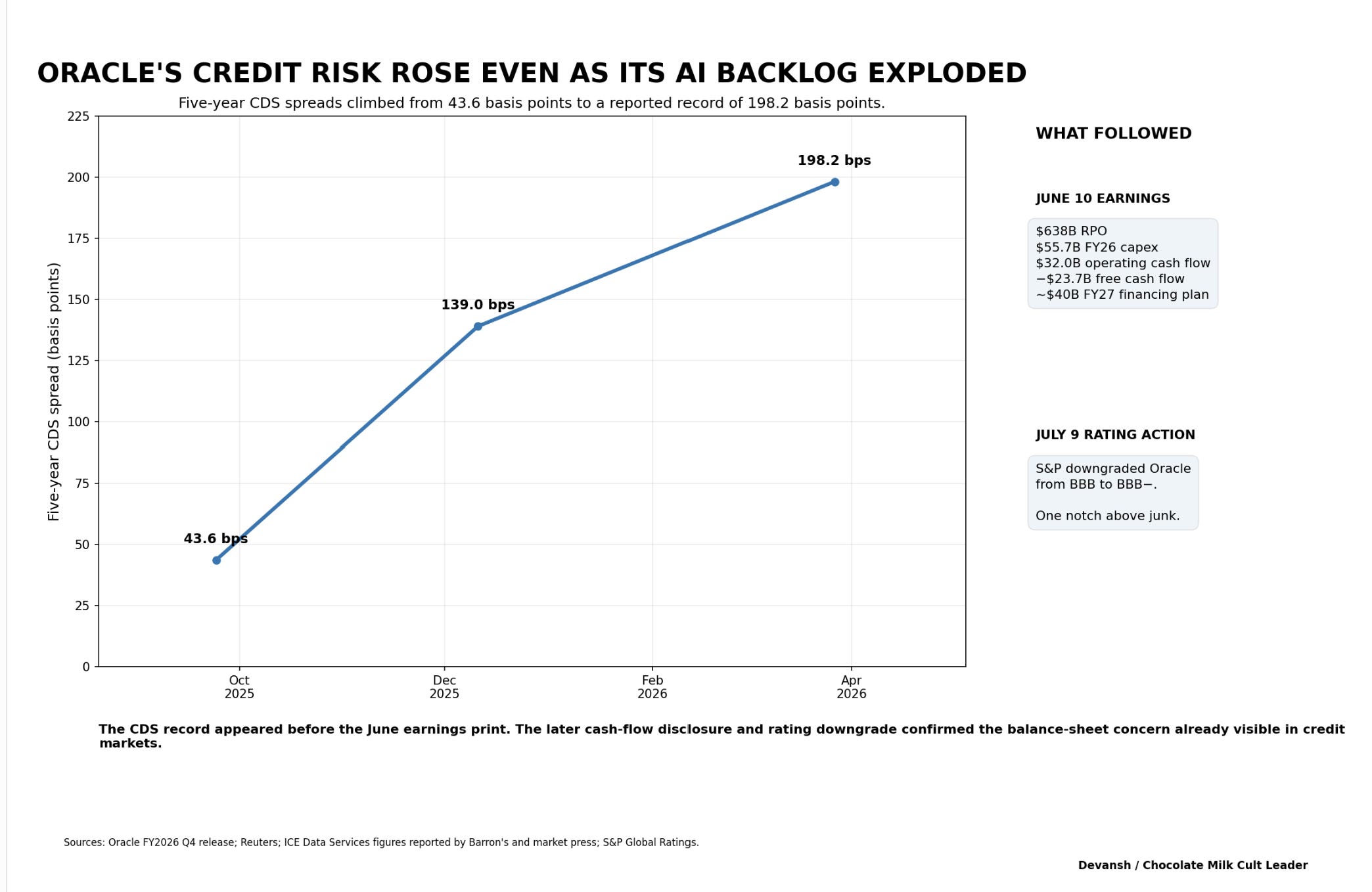

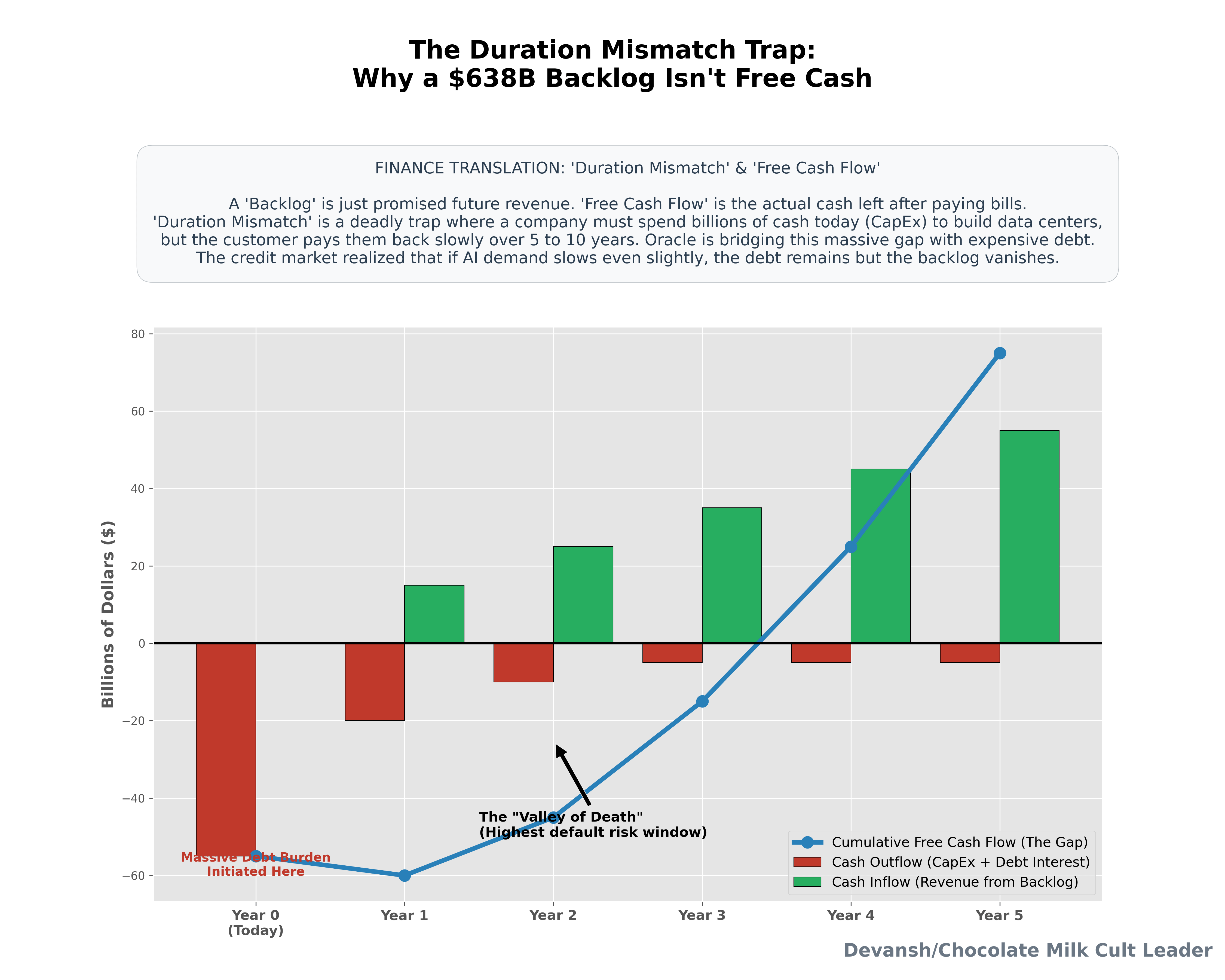

Oracle reported fiscal Q4 on June 10. Revenue reached $19.2B, up 21%; Oracle Cloud Infrastructure grew 93%; and remaining performance obligations reached $638B, up 363% year over year. On the old enterprise software scorecard, this was ridiculous. Oracle had produced what looked like the greatest earnings print in the industry’s history. But times are changin’ pretty fast.

So instead, the stock fell roughly 12% the next day.

Why?

Oracle spent approximately $55.7B on capital expenditure in FY26 and generated negative $23.7B of free cash flow. It raised $43B in debt and $5B in equity during FY26, then told investors it expected to raise another $40B through debt and equity in FY27.

Now, there is an important correction to the pure doom version of the story. Oracle said $75B of its large AI contracts involved customers either prepaying for GPUs or supplying the GPUs themselves. The entire $638B backlog is not an unfunded liability (which coincidentally is what my parents called me before I got a job; how proud Indian parents are of their son writing his newsletter instead of working for a respectable company is left to your imagination).

The problem is timing.

Oracle must build the infrastructure before most of the revenue arrives. It carries the financing, construction, utilization, depreciation, and counterparty risks in between. This is something that the credit market had already noticed. In March, Oracle’s five-year credit default swap spread reached a record of roughly 198 basis points, up from around 40 basis points one year earlier. The market was charging nearly five times as much to insure Oracle’s debt before the June results explained why.

Investors cannot independently verify the ultimate margins, utilization, cancellation risk, or counterparty durability embedded in $638B of long-dated contracts. They can verify $55.7B of capex, negative free cash flow, and another enormous financing requirement. So credit priced what it could see.

(July update: On July 9, S&P downgraded Oracle from BBB to BBB-, one notch above junk. S&P said Oracle’s expanding AI infrastructure business was weakening its traditional business-risk profile and admitted that it had underestimated how much investment the buildout would require. One of June’s proposed confirmation signals arrived within a month.)

The point here isn’t that Oracle is about to default. It is that Oracle is using its investment-grade balance sheet to bridge the gap between AI companies’ current cash flows and their future compute commitments.

OpenAI is the obvious concentration risk. They OpenAI burned $3.7B during the first quarter of 2026 against $5.7B of revenue. Reuters could not independently verify the internal documents, but the mismatch is large enough to show what Oracle is financing around. Oracle equity is therefore becoming a leveraged bet on more than AI demand. It depends on customers converting compute commitments into sufficiently profitable products before financing costs, depreciation, and infrastructure margins consume the upside.

If I am to put all of that simply, the 2-line takeaway is that while a backlog is traditonally seen as an asset, a backlog that requires tens of billions in financing before it pays is a …problem.

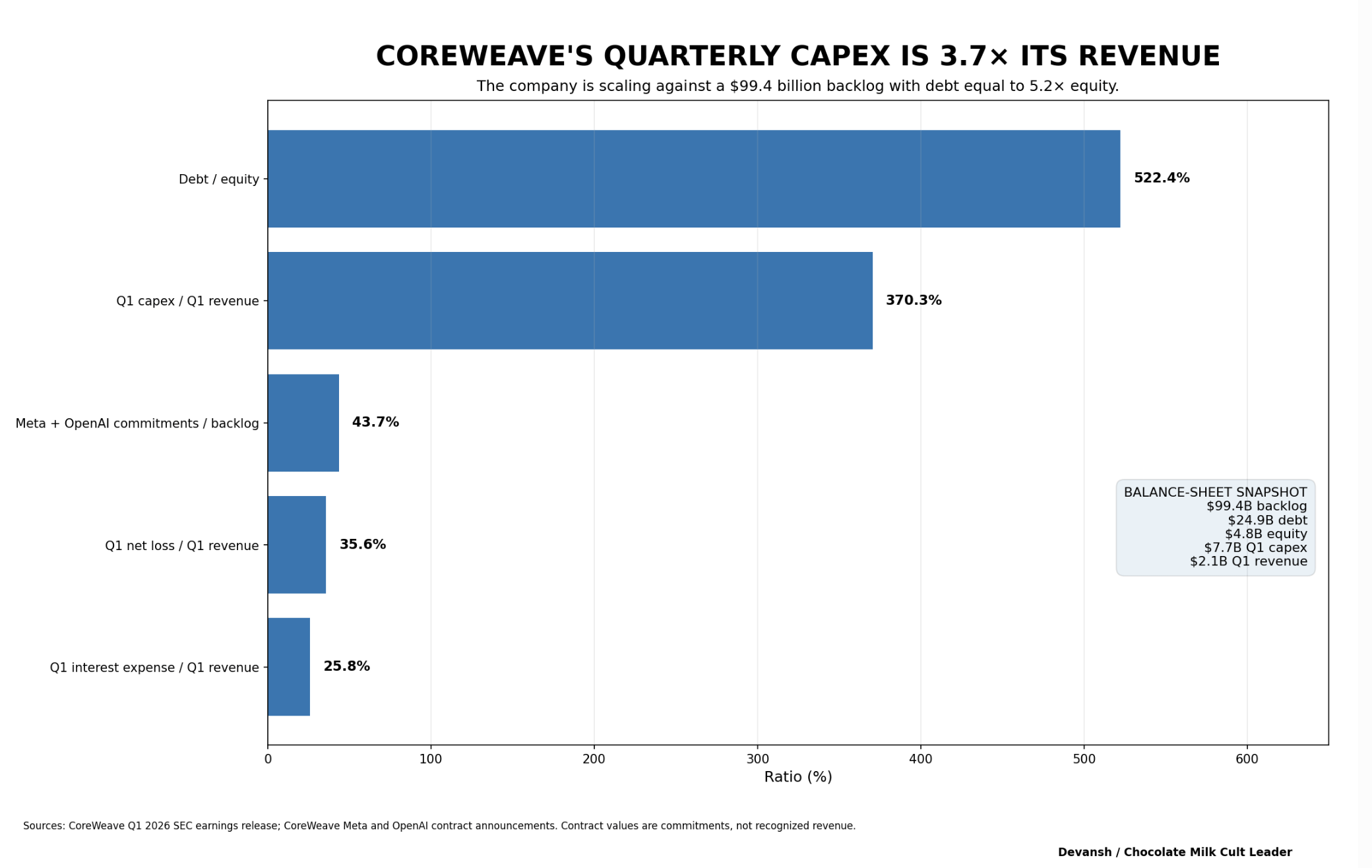

CoreWeave shows the same structure without Oracle’s software cash flows. It ended Q1 with $99.4B of revenue backlog and $2.08B of quarterly revenue, but recorded $536M of net interest expense and a $740M net loss. The company also signed a new $21B commitment from Meta and a multi-year agreement with Anthropic.

Again, demand is not the problem.

The company must finance GPUs, power, and data centers today against contracts recognized over several years. If delivery slips, utilization falls, customers internalize capacity, or refinancing costs rise, the backlog becomes less valuable. That is not good.

On June 28, the Bank for International Settlements finally named the structure. Its annual report warned that AI investment was increasingly being supported by debt and complex financing arrangements, while intense competition and infrastructure bottlenecks increased the risk of overinvestment followed by a prolonged investment bust. Reuters summarized the warning as a growing financial vulnerability created by high valuations and increasingly complex debt-financing structures.

The circularity became almost comically visible through SpaceX (god bless Elon). After SpaceX acquired xAI in February, Anthropic took the full capacity of the 300MW Colossus 1 data center. Google then agreed to pay SpaceX $920M per month from October 2026 through June 2029 for capacity including roughly 110,000 Nvidia GPUs.

The Anthropic and Google agreements carried a combined headline value of more than $70B over their stated terms. But headline value was not guaranteed revenue. Google could terminate after December 31 with 90 days’ notice and could exit earlier if SpaceX failed to meet its delivery obligations.

And that is AI financing in 2026. An AI lab rents compute from the parent company of a competing AI lab. The supplier records a massive contract. The customer records access to future compute. Outside investors see the headline value but cannot observe future utilization, contract durability, or the economics supporting either side.

Everyone gets a backlog.

The GPUs still have to earn the money. But that isn’t something we need to talk about. After all, who cares about profits when our benevolent tech oligarchs will solve all our society’s problems by making us dependent on their platforms? At that point, what is the alternative?

3.2. The Memory Oligopoly Learned What Unverifiable Capacity Is Worth

Everywhere else in June, verification arrived and prices corrected.

In memory, the margins showed what happens when verification remains weak.

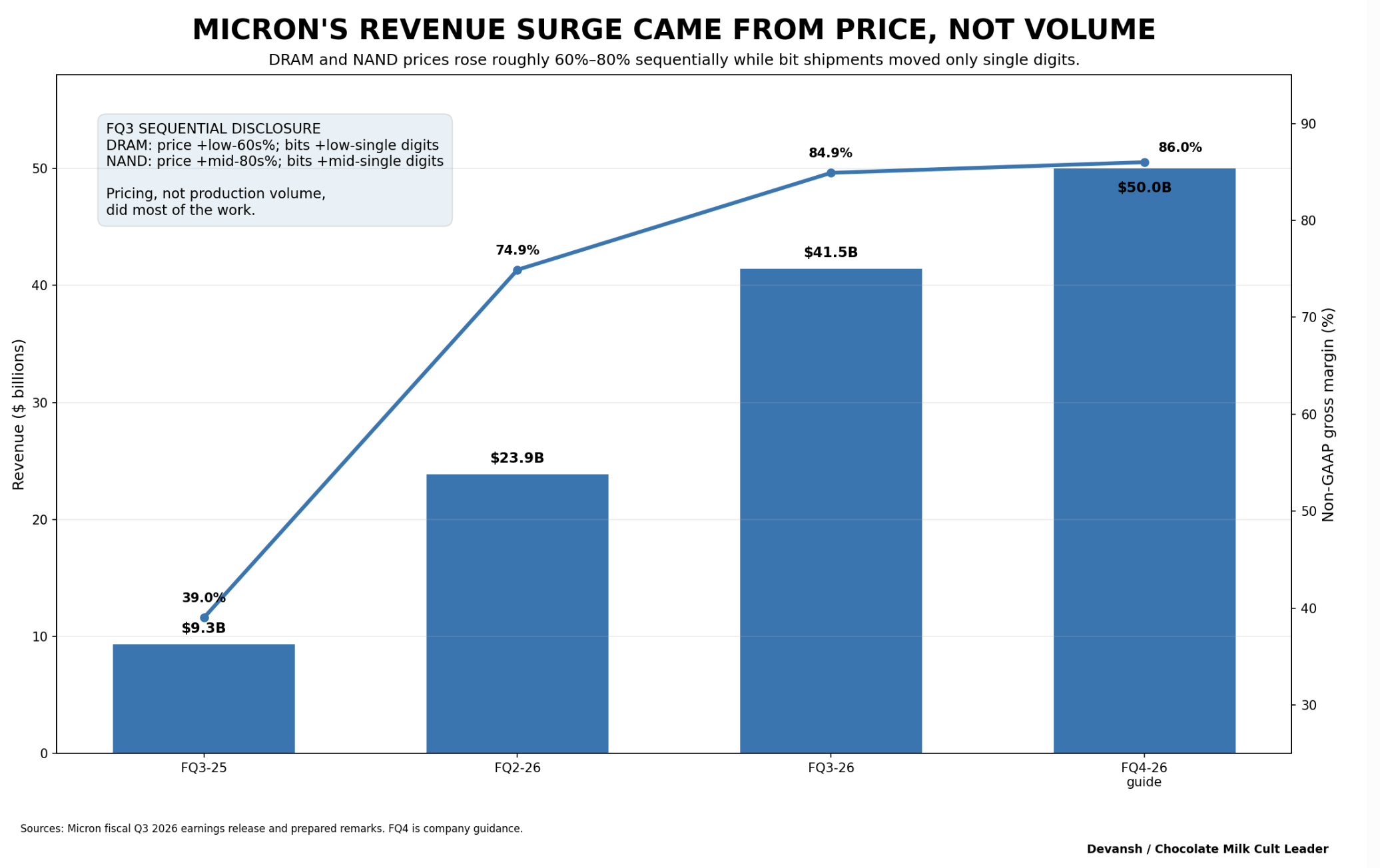

Micron reported fiscal Q3 revenue of $41.46B, up from $9.30B one year earlier. Its non-GAAP gross margin reached 84.9%, compared with 39% one year earlier. The company then guided to $50B of revenue and approximately 86% gross margin for the following quarter. Those are not ordinary commodity-cycle numbers. Micron’s core data-center business reported an 87% gross margin.

Micron also announced strategic agreements covering 16 customers and approximately $22B of commitments. The agreements included deposits, purchase obligations, and pricing protections intended to make the current shortage more durable and predictable for Micron.

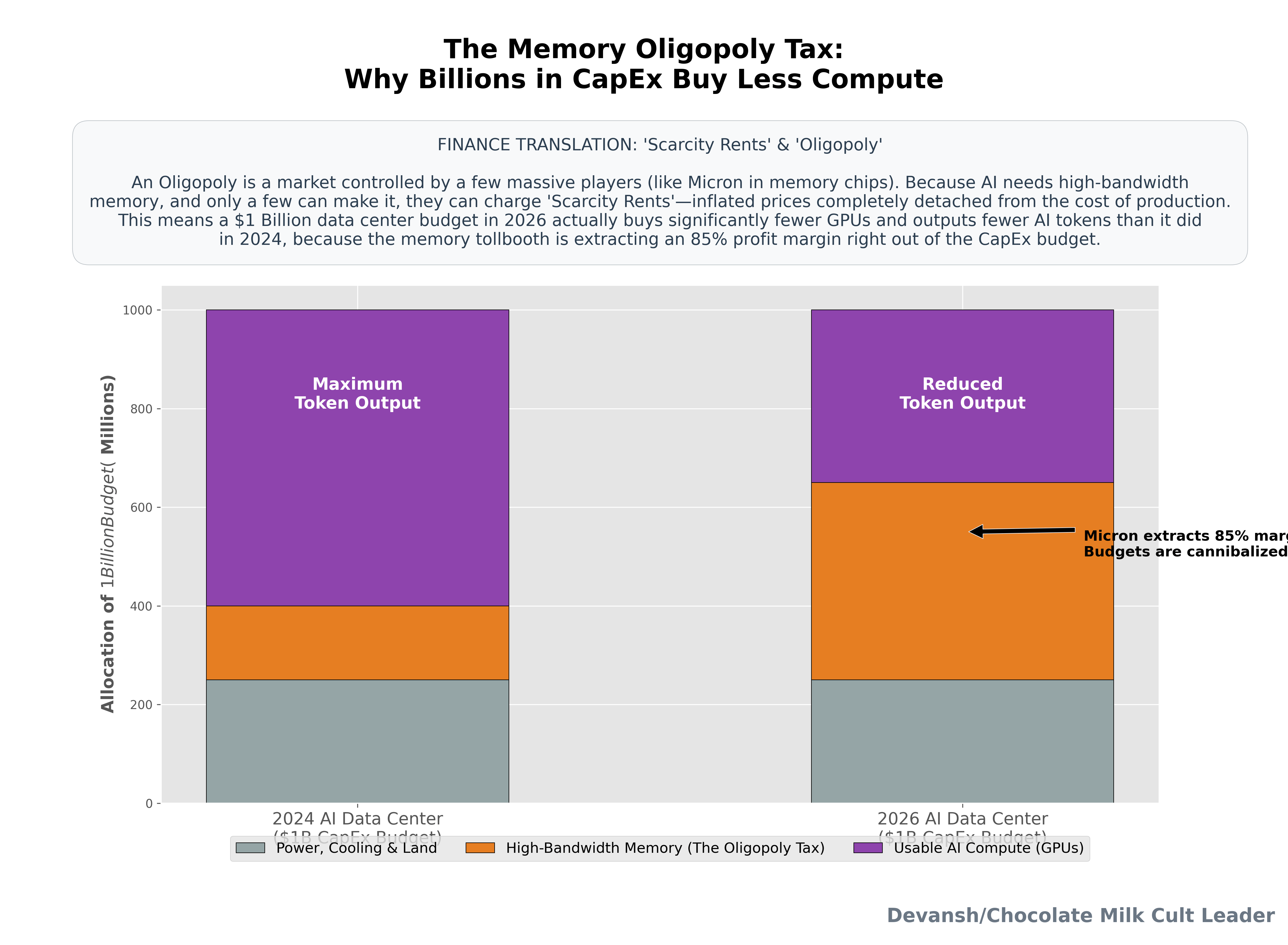

The shortage itself is real. AI systems require enormous quantities of high-bandwidth memory, while new fabrication plants and production lines take years to build and qualify.

What outsiders cannot verify is how much of the scarcity is unavoidable. Customers and analysts cannot independently observe manufacturers’ true wafer allocations, production yields, conversion schedules, or how aggressively each supplier could expand capacity at a lower margin. The manufacturers control the supply and most of the useful information about that supply. When supply is concentrated, capacity is opaque, and customers are desperate, suppliers can capture extraordinary scarcity rents without outsiders being able to distinguish physical constraint from commercial discipline.

Micron’s 85% margin is the receipt.

(July update: On July 10, SK Hynix’s chief executive said 2027 could bring the worst memory shortage in the industry’s history and that demand may continue exceeding supply beyond 2030.)

The consequence spreads through every AI capex forecast. A growing portion of infrastructure spending now goes toward higher memory prices rather than proportionally more usable compute.

The third repricing in the industry came through the macro data.

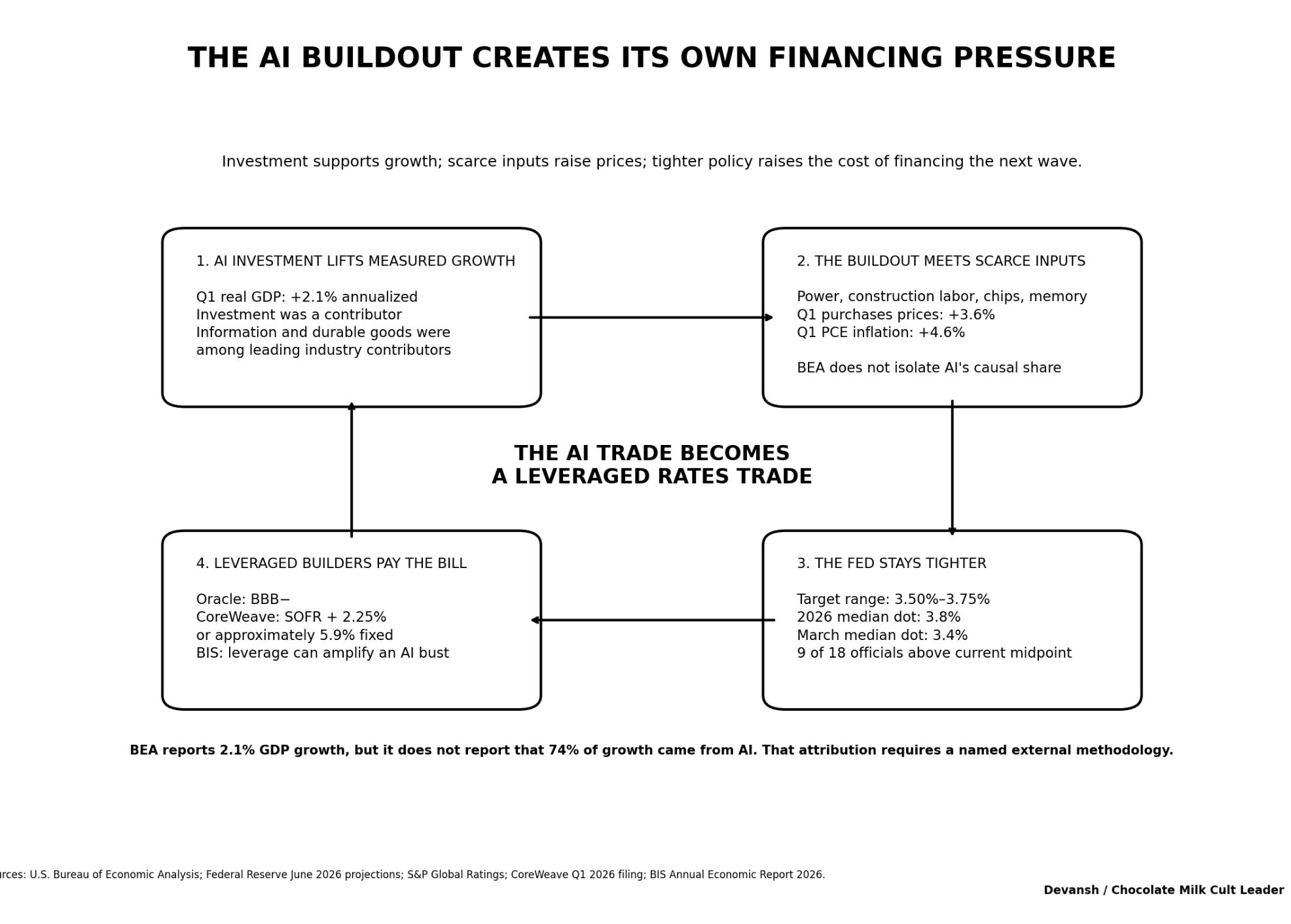

3.3. The Fed Discovered It Was Underwriting the Buildout

On June 25, the Bureau of Economic Analysis raised first-quarter real GDP growth to 2.1% annualized. Investment, information services, professional and technical services, and durable-goods manufacturing were among the major contributors. Meanwhile, real final sales to private domestic purchasers grew only 1.7%.

The BEA does not publish an official “AI contribution to GDP.” One private decomposition estimated that AI-related spending accounted for approximately 76% of first-quarter headline growth. That number depends heavily on which investment categories are labeled AI, so it should be treated as an estimate, not a national-accounting fact.

This means that AI infrastructure has become one of the main engines of American business investment at the same moment that underlying domestic demand was weakening.

Then on June 17, the Federal Reserve held its policy rate at 3.50% to 3.75%. But its projections turned sharply more hawkish. The median projected year-end 2026 rate rose to 3.8%, while the median 2026 PCE inflation forecast rose to 3.6% and core PCE to 3.3%.

Why are we talking about this? Simply put, this creates another kind of loop— AI capex supports economic growth. Stronger growth gives the Fed less room to cut. Higher rates then raise the financing cost of the infrastructure producing that growth.

The companies most exposed are not the cash-rich hyperscalers. They are Oracle, CoreWeave, and the rest of the leveraged layer being paid to build capacity for them.

The Nasdaq demonstrated the sensitivity on June 5. After the US economy added 172,000 jobs, more than twice the consensus estimate, expectations of another rate increase surged and the Nasdaq fell approximately 4.2%.

July update: The June inflation report, released on July 14, weakened the most aggressively hawkish version of this argument. Headline CPI fell 0.4% during June and rose 3.5% year over year, while core CPI was flat for the month and rose 2.6% over the year. That reduced the immediate probability of another increase, but it did not remove the underlying sensitivity of debt-funded infrastructure to interest rates.

There is also one necessary correction before the bears become drunk on their own seriousness.

The viral claim that half of planned 2026 US data-center capacity had been canceled was wrong. Dylan Patel found that its forecast for genuine hyperscaler self-build capacity had changed by only around 1% over six months, while its colocation forecast moved by less than 5%.

The apparent collapse came from counting speculative announcements as real projects. Many lacked financing, tenants, equipment orders, interconnection agreements, or construction. In other words, they weren’t really serious projects to begin with.

Demand remained enormous during the same month the credit warnings arrived. Broadcom forecast $16B of AI-chip revenue for fiscal Q3, more than triple the year-earlier level, although the forecast still fell slightly below Wall Street’s expectations. OpenAI had also committed to purchasing up to 750MW of Cerebras capacity, with the expanded agreement reportedly valued above $20B.

Whether this buildout produces enough revenue to justify the capital depends on whether customers continue paying for the agents consuming all this compute. June gave us plenty to examine there.

Section 4. How CFOs Started Metering AI Agents

We’ve been talking about the breakdown of flat-rate agent pricing for a while now. June showed the two replacements: charge customers for the compute agents consume, or charge for outcomes and make the vendor absorb the cost of failure.

4.1. Input Metering Versus Outcome Pricing

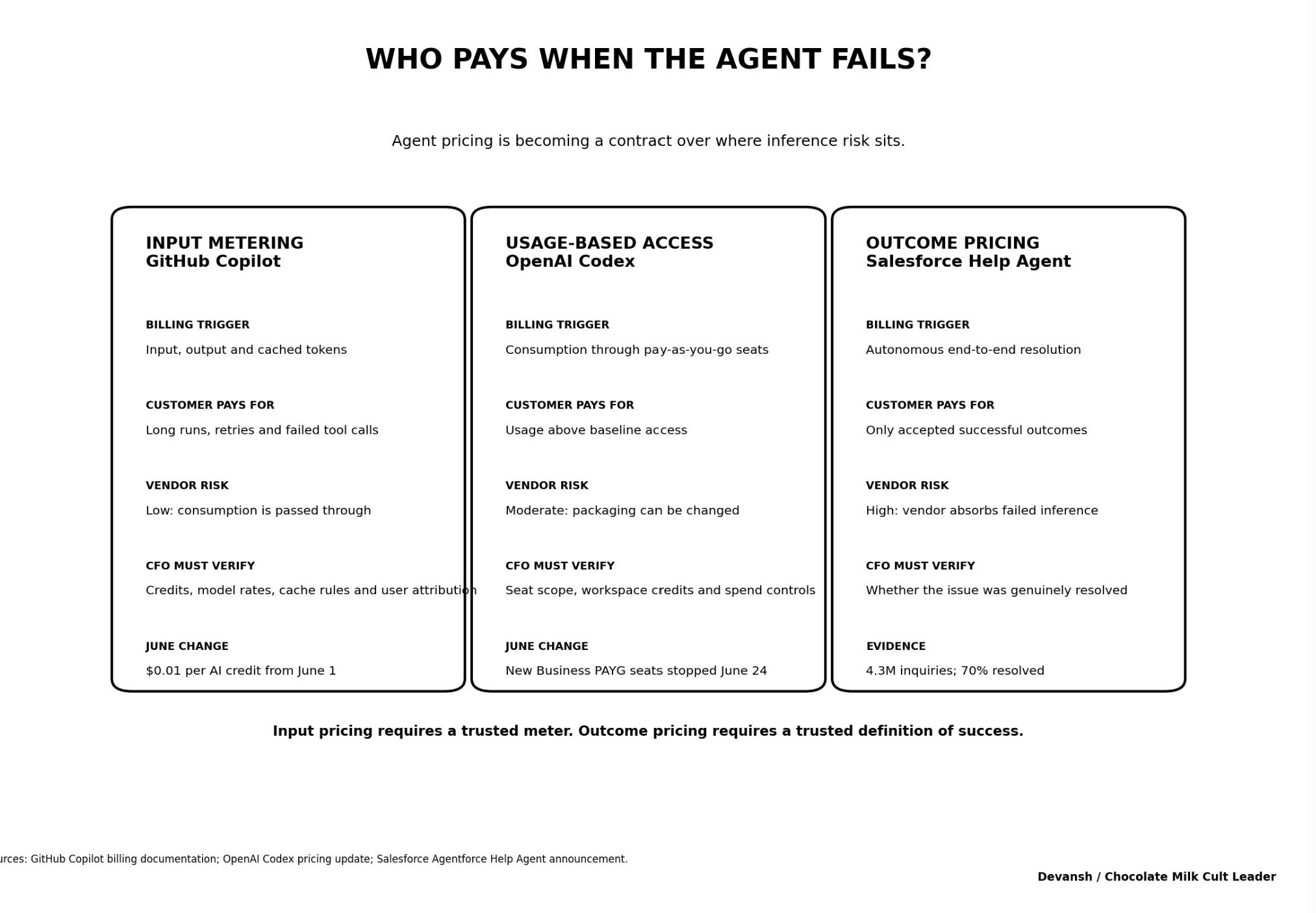

On June 1, GitHub replaced Copilot’s premium-request system with GitHub AI Credits, priced at $0.01 per credit and calculated from the input, output, and cached tokens consumed at each model’s API rate. GitHub’s explanation was blunt: under the old system, a short chat request and a multi-hour autonomous coding session could cost the user the same amount, leaving GitHub to absorb the difference, which agentic usage had made “no longer sustainable.”

The base subscriptions remained at $10 per month for Copilot Pro, $19 per user for Business, and $39 for Enterprise, but usage above the included allowance became the customer’s problem, including failed searches, repeated test runs, bad tool calls, and retries. Some users reported projected bills up to 100 times higher, although these were individual reports rather than audited platform-wide data. GitHub added per-user credit consumption to its usage metrics API on June 19 and, by July 2, introduced cost-center credit pools and separate spending caps.

OpenAI moved in the same direction, then partially reversed course. It introduced pay-as-you-go Codex seats for Business and Enterprise customers in April, then stopped offering new pay-as-you-go seats to ChatGPT Business customers on June 24. Existing seats remained active and normal Business subscriptions still included baseline Codex access, but the self-serve path from experimentation to metered deployment lasted less than three months.

Finally, Salesforce took the opposite side of the risk. Its Agentforce Help Agent, launched on June 25 with pay-per-resolution billing scheduled for July, charges only when an issue is resolved autonomously from beginning to end, with no charge when the customer gives negative feedback or requests a human. Salesforce did not publish the per-resolution price in June, but the structure matters more than the number: under input pricing, the customer pays while the agent tries; under outcome pricing, the vendor absorbs the inference cost and gets paid only when it can defend the result as successful.

Salesforce says its own Help site has processed 4.3 million inquiries and autonomously resolved 70% of them, but outcome pricing does not remove verification; it relocates it. Every disputed resolution becomes a billing argument over whether the issue was genuinely closed, whether the user returned, whether a human corrected the answer, and who defines success. Watch every dispute require a 46-page submission of proof, so that most unhappy customers are annoyed into not submitting claims. Such is the nature of progress after all.

Both approaches exist because agents broke the core SaaS assumption that consumption per seat is bounded by human attention. Ramp’s June transaction data showed the resulting spread: across more than 70,000 US businesses, median AI spending was only $11.38 per employee per month, while the top 10% spent roughly $611 and the top 1% spent $7,449. Flat-rate pricing works on the median customer and collapses around the most aggressive users (and as more expensive models become common + more people start using agents, the cost percentiles will shift a lot).

4.2. The Month Demand Learned to Say No

The stronger signal came from buyers:

Uber reportedly exhausted its full-year Claude Code budget during the first four months of 2026 and responded by imposing a $1,500 monthly limit per employee for each agentic coding tool, including Claude Code and Cursor.

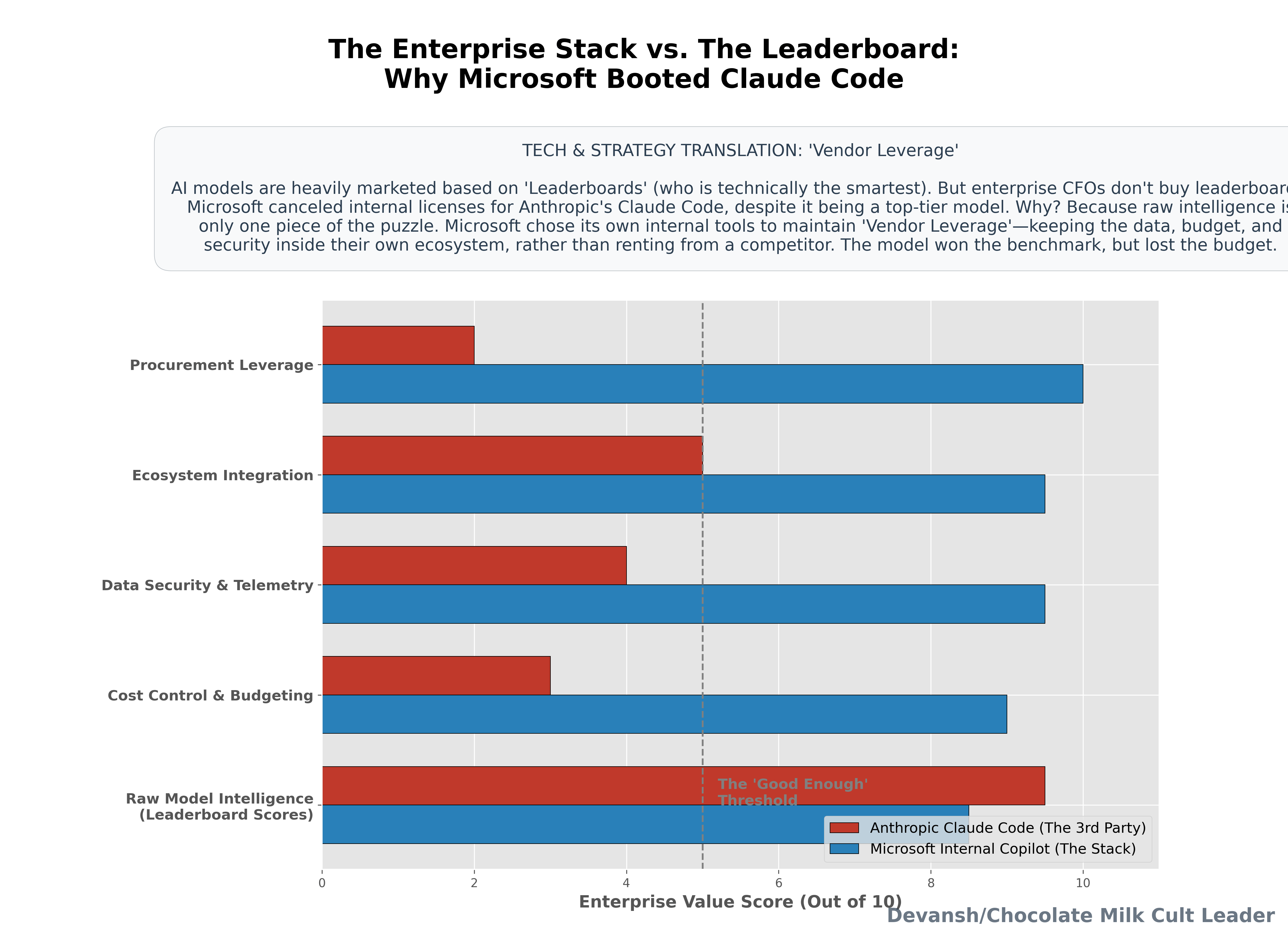

Microsoft offered the more revealing case. Its Experiences and Devices division, which includes Windows, Microsoft 365, Teams, Outlook, and Surface, began canceling most internal Claude Code licences and instructed thousands of employees to move to GitHub Copilot CLI by June 30. Claude models remained available through Copilot; Microsoft removed the separate Claude Code product and consolidated usage onto infrastructure, procurement, and telemetry it controlled.

The decision shows why enterprise buying isn’t as output-dependent as originally thought. A product can improve output and still lose the contract if the buyer owns a close substitute, can integrate it more deeply, and prefers to keep the data, spend, and bargaining power inside its own stack. A Microsoft study released in July found that engineers adopting command-line coding agents merged roughly 24% more pull requests over four months, although the authors warned that merged pull requests are only a proxy for value. Microsoft had internal evidence of measurable productivity gains and still removed most Claude Code licences because it did not need to rent Anthropic’s full product to capture them.

Once costs become visible, enterprises optimize across performance, integration, security, procurement, observability, switching costs, and vendor leverage rather than simply buying whichever model tops a leaderboard. The model can win the benchmark while the vendor loses the budget.

The spending data shows the same pattern. A January survey of 100 Global 2000 executives found that average enterprise LLM spending had risen from about $4.5M to $7M over two years, with respondents expecting another 65% increase during 2026, while 81% were testing or using at least three model families and 65% still preferred incumbent products when available. Budgets were growing, but they were also becoming fragmented, governed, and negotiable. Falling token prices did not produce infinite demand because cheaper intelligence still had to pass through procurement.

4.3. The Tokenizer Became a Pricing Weapon

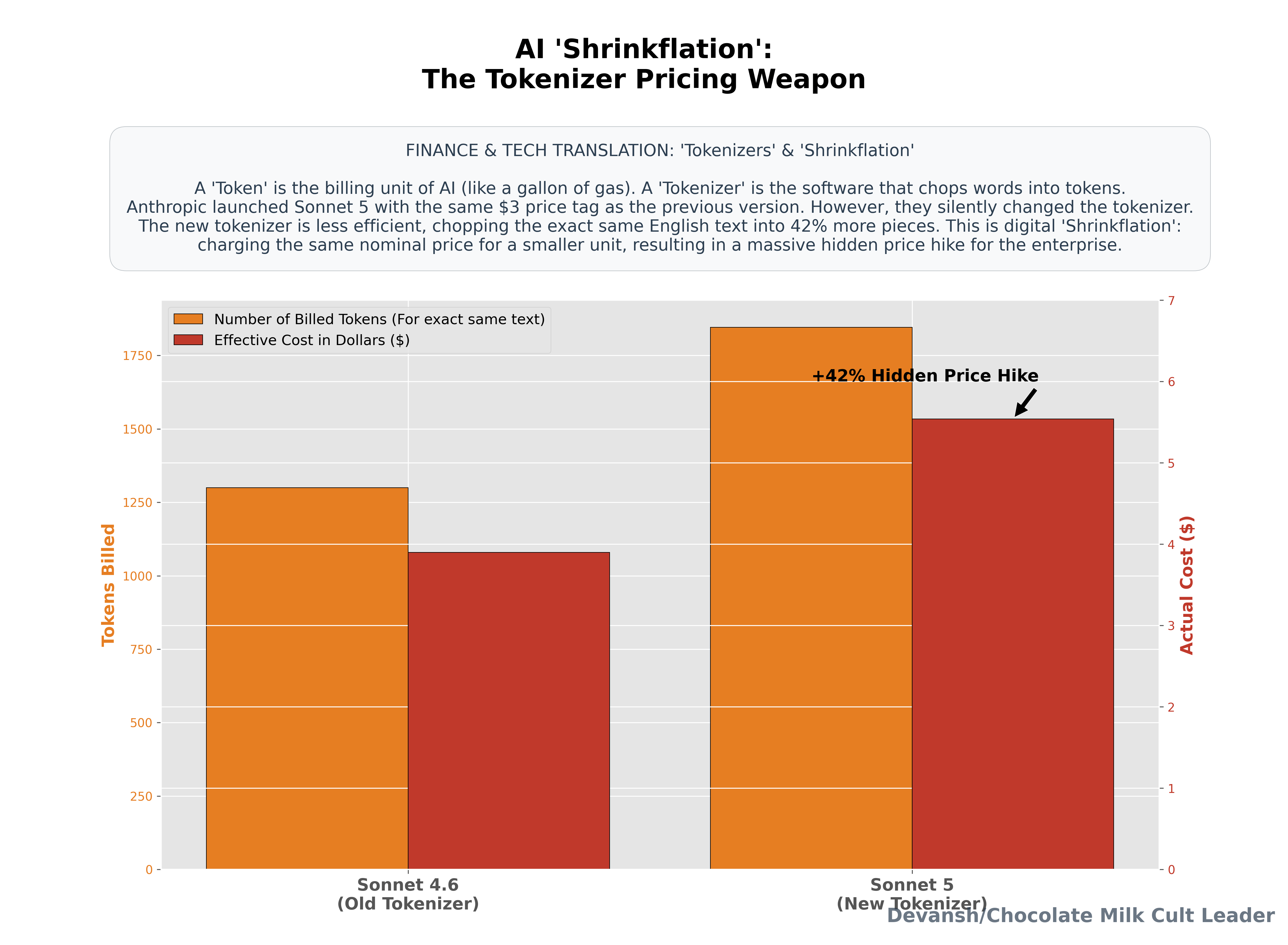

Once buyers began auditing the bill, the billing unit itself became unstable. Anthropic launched Claude Sonnet 5 on June 30 at an introductory $2 per million input tokens and $10 per million output tokens through August 31, rising to $3 and $15 afterward. Sonnet 5 also introduced a new tokenizer that, by Anthropic’s own estimate, produces approximately 30% more tokens than Sonnet 4.6 for the same input, depending on the content.

Simon Willison’s independent testing found that identical documents produced 1.42 times as many tokens for English, 1.33 times for Spanish, 1.27 times for Python, and almost no change for Simplified Mandarin. On the English sample, the promotional rate therefore translates to an effective $2.84 per million old-token-equivalent input tokens and $14.20 for output, roughly matching Sonnet 4.6’s $3 and $15 pricing. Once the promotion ends, the same text costs an effective $4.26 and $21.30, a 42% increase despite an apparently unchanged price card.

Anthropic disclosed the tokenizer change, so the problem is not concealment. The problem is that vendors trained customers to treat tokens as a common unit while retaining the power to redefine the unit. Dollars per million tokens is not comparable across vendors if one tokenizer turns the same document into 42% more billable units.

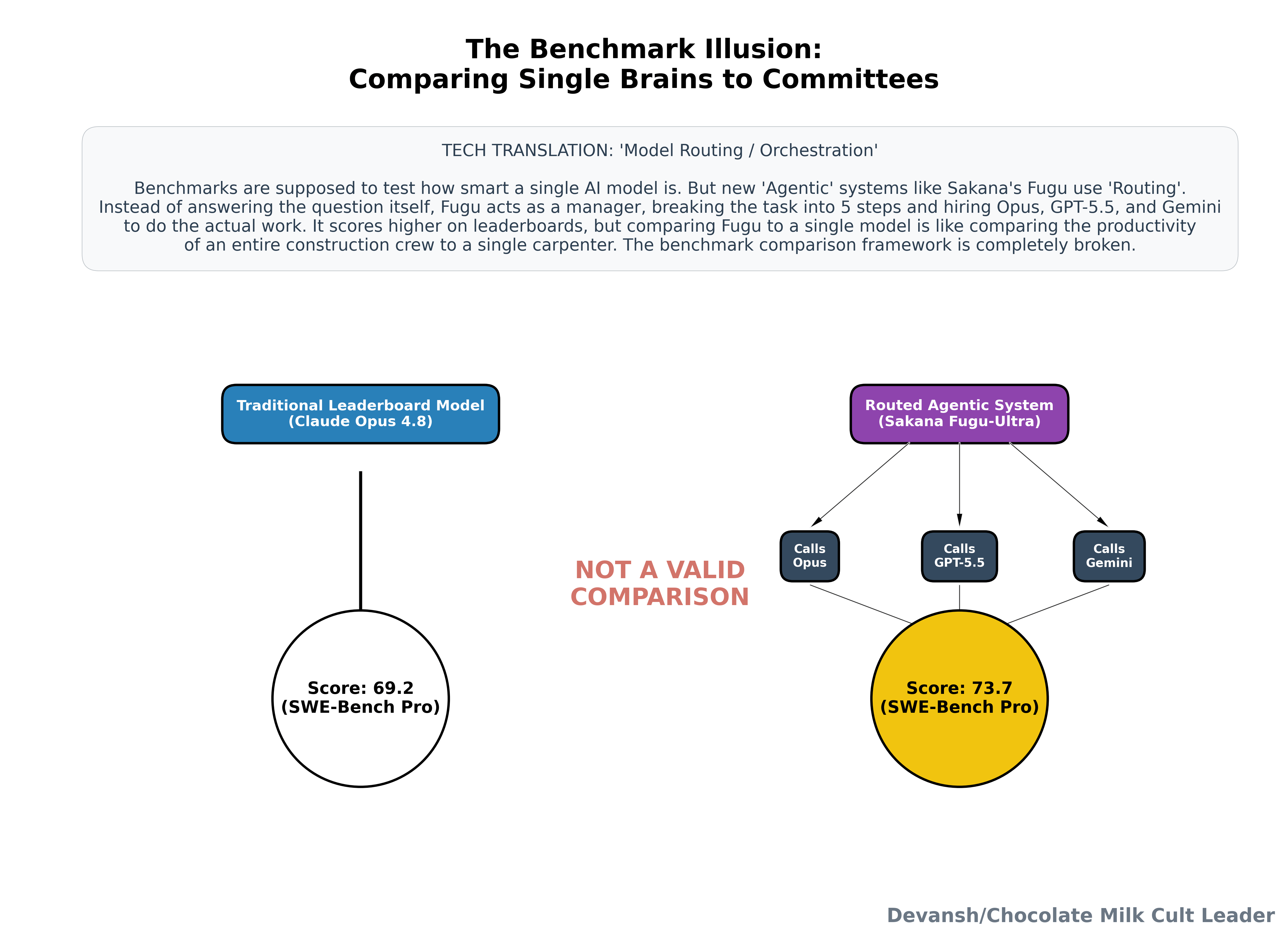

The comparison breaks further when the product label no longer identifies one fixed model. Anthropic’s Fable 5 can route certain risky requests to Opus 4.8, while Sakana’s Fugu-Ultra orchestrates Claude Opus 4.8, GPT-5.5, and Gemini 3.1 Pro through workflows of up to five steps. Fugu reached 73.7 on SWE-Bench Pro against 69.2 for Opus 4.8, not because Sakana trained a single superior base model, but because its router could buy work from several frontier models and combine the results.

That is a legitimate result, but it makes the current comparison framework useless. Benchmarks assume one model answered, price cards assume tokens are comparable, and leaderboards assume test-time compute is bounded or disclosed. Agentic systems can violate all three assumptions at once through routing, retries, hidden reasoning, tool use, and variable compute.

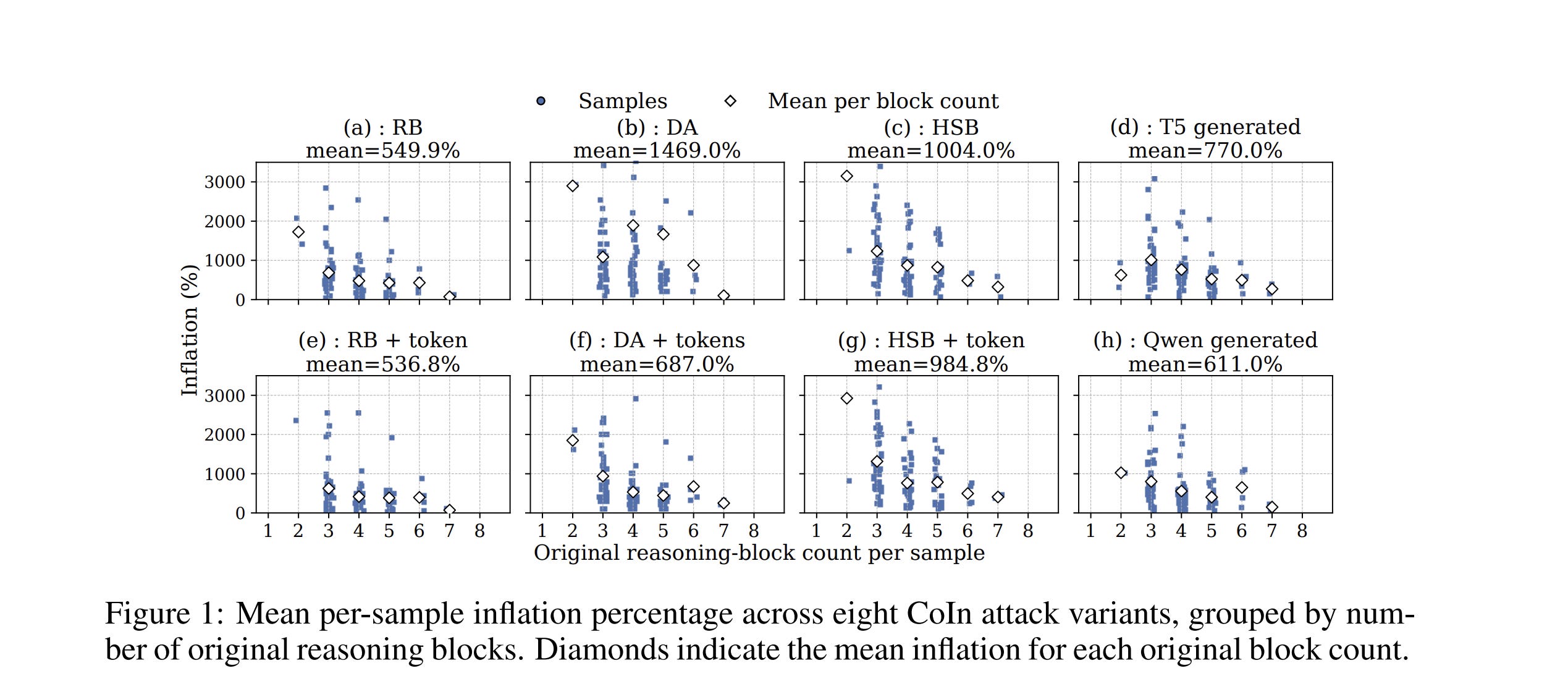

Thus, the only useful comparison is cost per successfully completed task, normalized for the tokenizer and accompanied by the full execution record: models called, retries, cached and uncached context, tools used, human intervention, and failure rate. Even that is difficult because vendors control most of the evidence. A May paper on token billing found that tokenizer ambiguity permitted 50.85% over-reporting below the detection threshold in simulated attacks, while hidden-reasoning inflation reached 1,469% in the most permissive setting.

This means that while a developer could detect Sonnet 5’s tokenizer change with a script, an enterprise audit layer must repeat that exercise continuously across tokenizers, routers, hidden reasoning, tool calls, cache rules, discounts, retries, and outcome definitions. The standards-and-audit market is therefore an attempt to build a trusted meter for a product whose manufacturer controls the ruler.

Credit desks were pricing the buildout, and CFOs were pricing the agents. Buyers then moved more volume toward models that were cheaper, easier to inspect, and harder to switch off.

Section 5. Why Open-Weight Models Took the Token Volume

On June 12, the Commerce Department forced Anthropic to disable Fable 5 and Mythos 5 because it could not verify users’ nationalities in real time. Both models disappeared globally on June 12. Mythos 5 partially returned for vetted US critical-infrastructure operators on June 26, Commerce revoked the directive on June 30, and Fable 5 returned globally on July 1. Four days after the shutdown, Z.ai released GLM-5.2 under an MIT licence, with downloadable weights and no regional lock.

That contrast explains most of the open-weight strategy. A hosted model remains controlled by its developer, cloud provider, and home government. Access can be restricted, prices can change, usage can be monitored, and the service can disappear without the customer’s consent. Once open weights have been downloaded and deployed on private infrastructure, no vendor can remotely disable them or rewrite the terms of access. For buyers outside the United States, particularly governments and regulated companies, that is not an ideological preference for open source. It is supply-chain control.

Open weights are also easier to verify. Customers can test the exact model version they will deploy, inspect its outputs across their own workloads, measure its real cost, control the inference environment, and reproduce results without depending on a vendor’s changing API. This does not make the system fully transparent; the training data and complete training process may still remain closed. But it removes several of the largest sources of uncertainty at deployment: hidden model changes, undisclosed routing, shifting tokenizers, regional restrictions, and vendor-controlled usage logs. In a market increasingly organized around auditability, the ability to hold the weights is itself a verification advantage.

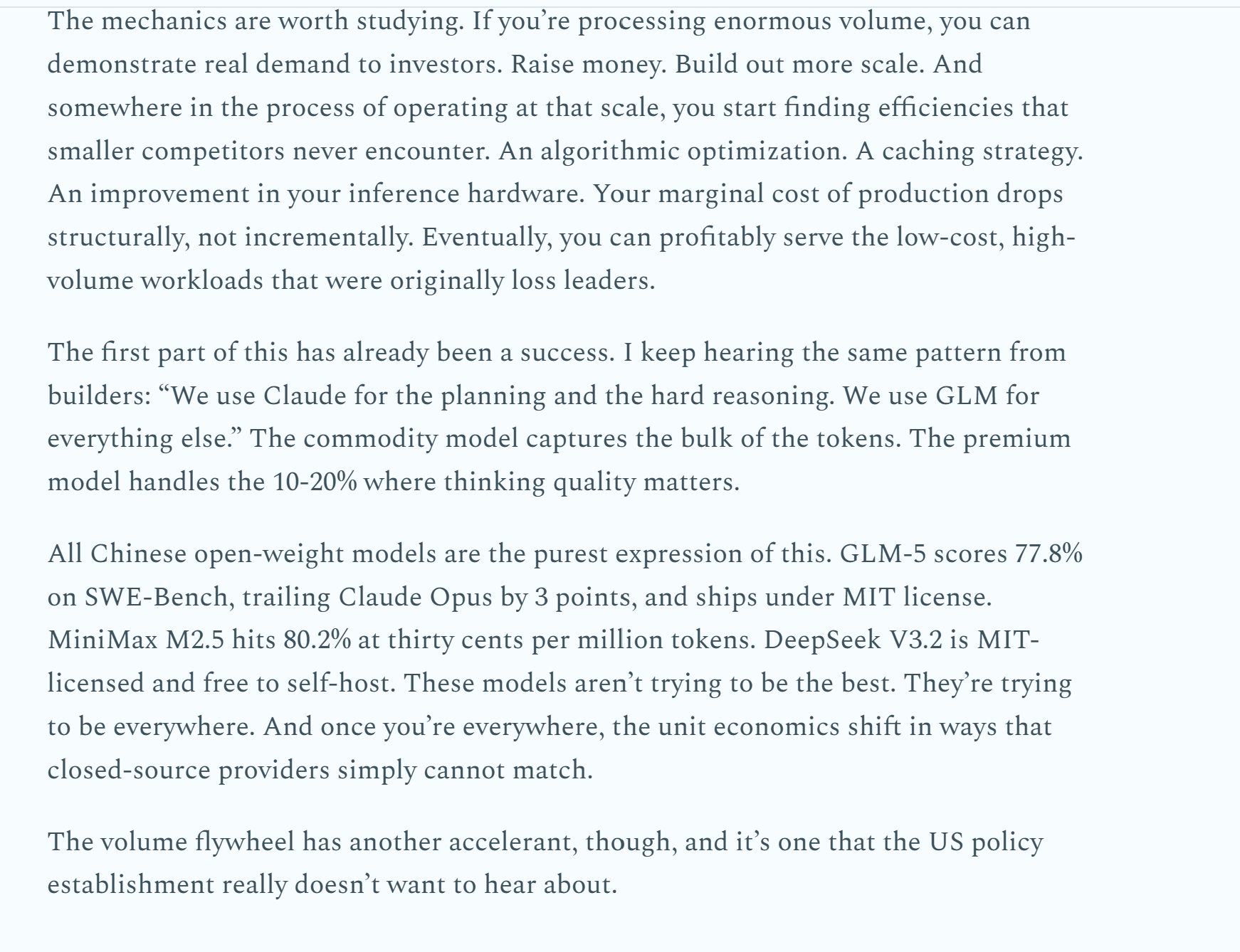

The economics then make the decision easier. OpenRouter found that Chinese models had overtaken US models in token volume by early June. Vercel’s June production data showed open-weight models handling 29% of tokens while accounting for less than 4% of spending. DeepSeek alone reached 22.6% of token volume, while proprietary models continued to dominate spending and the most sensitive workloads. The market was not replacing the frontier; it was dividing the work. Proprietary US models retained the tasks where the final increment of capability justified the premium, while cheaper open-weight models absorbed the repetitive, high-volume layer underneath. FYI— we called out how China was explicitly investing in their models to handle this “good intelligence, at low prices” segment (90% of the token volume) all the way back in Feb, as you can see below—

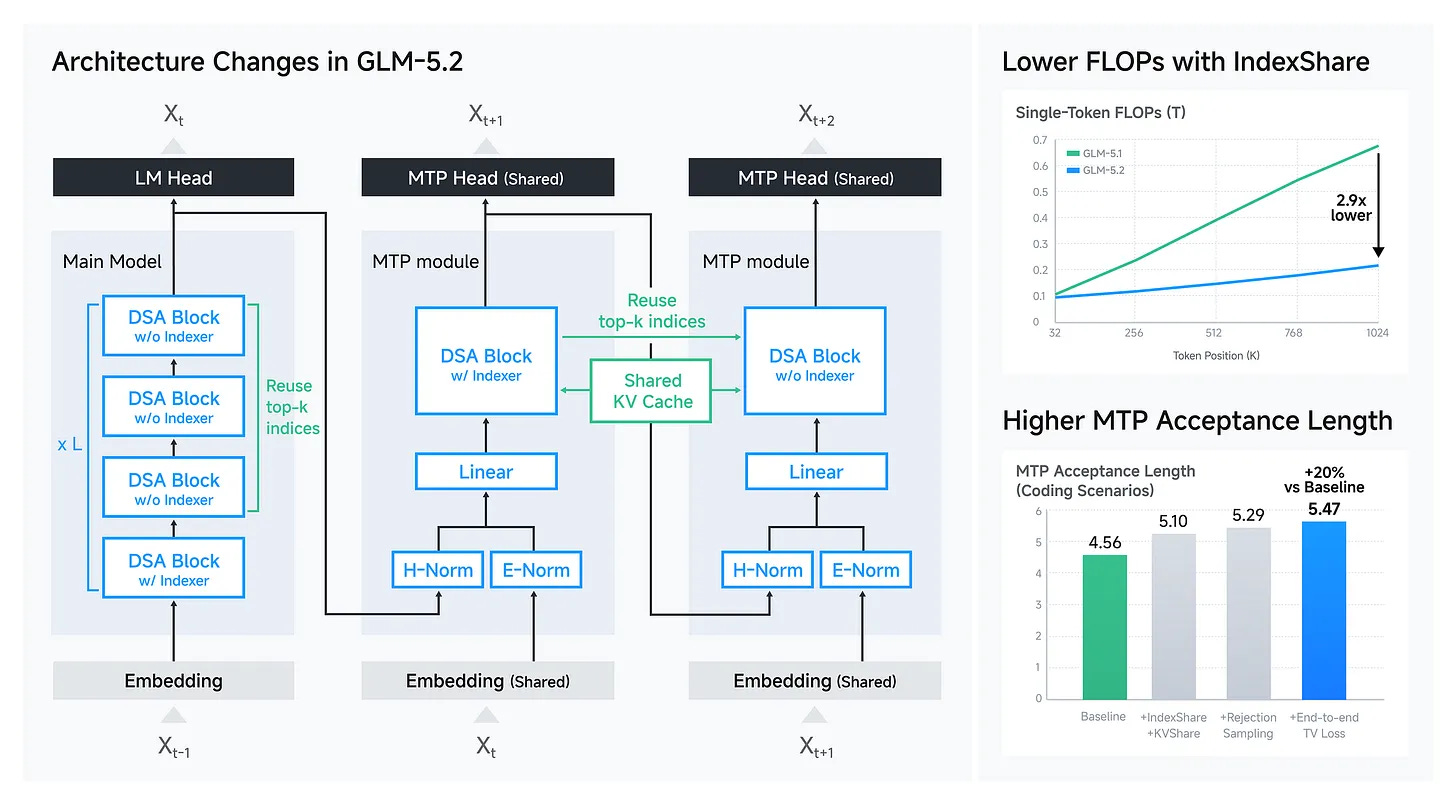

GLM-5.2 showed how quickly that layer could improve. Z.ai kept the same 744B-parameter mixture-of-experts architecture, with 40B active parameters per token, but generated a large performance gain through reinforcement learning, long-context training, distillation, and inference optimization rather than another increase in model size. This matters because the frontier premium now decays faster: once a capability becomes reproducible through post-training, an open model can offer most of it at a fraction of the price and without the vendor dependency. More on how GLM 5.2 accomplishes frontier performance at fractional costs here.

That is the strategic problem for American labs and export-control policymakers. Closed models are easier to regulate, but every restriction makes open weights more valuable to buyers who care about continuity, sovereignty, and verification. Washington can control access to an American API. It cannot recall a model already running on private infrastructure across Europe, India, or the Gulf.

The American frontier remains more capable at the top end, but it is closed, expensive, and permissioned. Chinese open-weight models are increasingly setting the price for everything below that frontier. In a market moving toward verification, the model a customer can inspect, host, and keep may be worth more than the model that scores slightly higher but can be switched off from somewhere else.

What Happens Next

Most enterprise decisions are exercises in avoiding blame.

For a while, benchmarks gave buyers cover. You chose the model at the top of the leaderboard, and if it failed, at least you had followed the numbers. That excuse is becoming harder to use. Benchmarks can be trained against, token prices are not comparable, routers hide how much compute was used, and the best model can still be the wrong commercial product.

Something else will replace them.

That is why verification matters. Audits, approved evals, cost-per-task measurements, trusted-partner status, public margins, and deployment records will become the new evidence buyers hide behind. None of these measures will be perfect. They do not need to be. They only need to make the decision defensible.

This gives power to whoever controls that evidence. Governments decide which models are cleared. Clouds decide which models are bundled, routed, and discounted. Enterprise platforms control usage data and procurement. Auditors decide what counts as safe or effective. The model lab may build the intelligence, but someone else increasingly decides whether it can be bought, how its value is measured, and where it gets deployed.

The labs wanted intelligence to become the platform underneath every industry. The disrupters that would bring the hallowed silicon valley efficiency and pioneering spriti to every segment of the world. They may instead become suppliers inside platforms controlled by governments, clouds, and enterprise software companies.

Life really has a funny sense of humor, doesn’t it?

Thank you for being here, and I hope you have a wonderful day,

Dev <3

If you liked this article and wish to share it, please refer to the following guidelines.

That is it for this piece. I appreciate your time. As always, if you’re interested in working with me or checking out my other work, my links will be at the end of this email/post. And if you found value in this write-up, I would appreciate you sharing it with more people. It is word-of-mouth referrals like yours that help me grow. The best way to share testimonials is to share articles and tag me in your post so I can see/share it.

Reach out to me

Use the links below to check out my other content, learn more about tutoring, reach out to me about projects, or just to say hi.

Small Snippets about Tech, AI and Machine Learning over here

AI Newsletter- https://artificialintelligencemadesimple.substack.com/

My grandma’s favorite Tech Newsletter- https://codinginterviewsmadesimple.substack.com/

My (imaginary) sister’s favorite MLOps Podcast-

Check out my other articles on Medium. :

https://machine-learning-made-simple.medium.com/

My YouTube: https://www.youtube.com/@ChocolateMilkCultLeader/

Reach out to me on LinkedIn. Let’s connect: https://www.linkedin.com/in/devansh-devansh-516004168/

My Instagram: https://www.instagram.com/iseethings404/

My Twitter: https://twitter.com/Machine01776819